The Indian banking and financial sectors encounter problems with unnecessary rules, inoperative banks and unequal access. Strong changes in governance, digital finance and regulation are needed for the economy and society to be stable and expand.

Since 1991, there have been big changes in India’s financial industry, but certain problems still call for immediate improvements. Even though past policies brought stabilization and growth in the banking industry, difficult regulations, inefficiency and the lack of financial access still slow down movement forward. Banks are confronted by challenges linked to NPAs, problems with governance and problems in adopting digital technologies. In addition, fintech innovations come up against rules that are no longer relevant, causing things to happen more slowly. Because of economic and financial changes around the world, India needs to address its system gaps, update its banks and rules and guarantee everyone can access financial services. A strong government, good rules and progress in technology will be important for forming a reliable and modern financial system. Making important, anticipated changes is important at this stage, to ensure financial security and growth for the economy and all its citizens. The article examines the crucial challenges in India’s financial space, recommends ways to resolve them and presents a guide to a better-organized sector.

India’s Financial Sector Reforms

Over the decades, significant transformations in India’s financial sector have been led by both economic needs and international trends. To understand these reforms, you must look at the important moments that changed the sector.

Before Liberalization

Until 1991, the government controlled most of the rules in India's financial sector. In 1969 and again in 1980, financial stability was reached, yet competition and efficiency declined after banks were taken over by the government. Limits on the interest rates, credit provided and foreign investments held back financial growth and caused the sector to remain stagnant.

1991 Reforms of Liberation

A major change in financial policy was triggered by India’s balance of payments issue in 1991. It was the Finance Minister who advised the government on the major reforms. To achieve this, the government made it possible for private banks, made borrowing credit easier, set interest rates free to move, and welcomed investors from other countries into financial services. This was when the financial industry started to be led by market forces.

Reforms in Banking and Capital Markets

The changes in the 1990s meant there was more competition and, as a result, private banks such as HDFC and ICICI entered the market. RBI introduced various steps to boost banking efficiency, raise the strength of banks’ capital and manage risks better. Besides, part of the capital market reforms included establishing SEBI, which made investors safer and the market more transparent.

Developments in technology and the Fin-tech

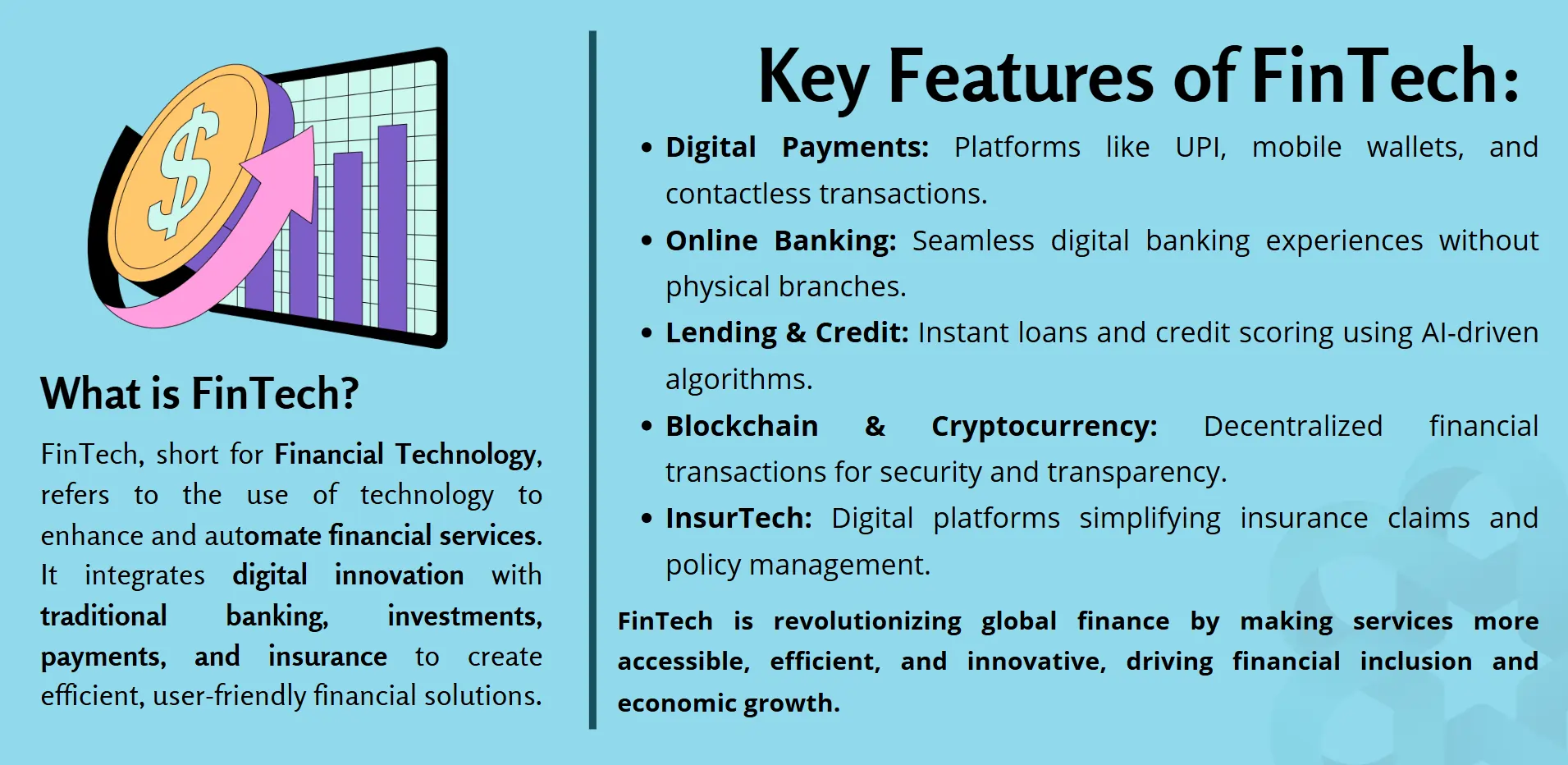

During the 2000s, banks and fintech firms began to use technology more than ever before. Due to electronic fund transfers, online banking and mobile payments, the financial industry has changed a lot. Efforts made by the government such as Aadhaar-linked banking and UPI, guided more people to digital financial services and made banking transactions less time-consuming and easier.

Present Problems

While these advances have come about, NPAs, flaws in banking governance and complex regulations are still problems within the industry. While previous changes offered a solid base, India’s financial sector should continue to modernize to meet new global needs and solve domestic problems that remain.

Current State of India’s Finance Sector

Because of earlier reforms, India’s financial industry now confronts both old and new obstacles and possibilities. Growth in Australia has come from digital and policy progress, but some problems with efficiency persist.

Growth and stability

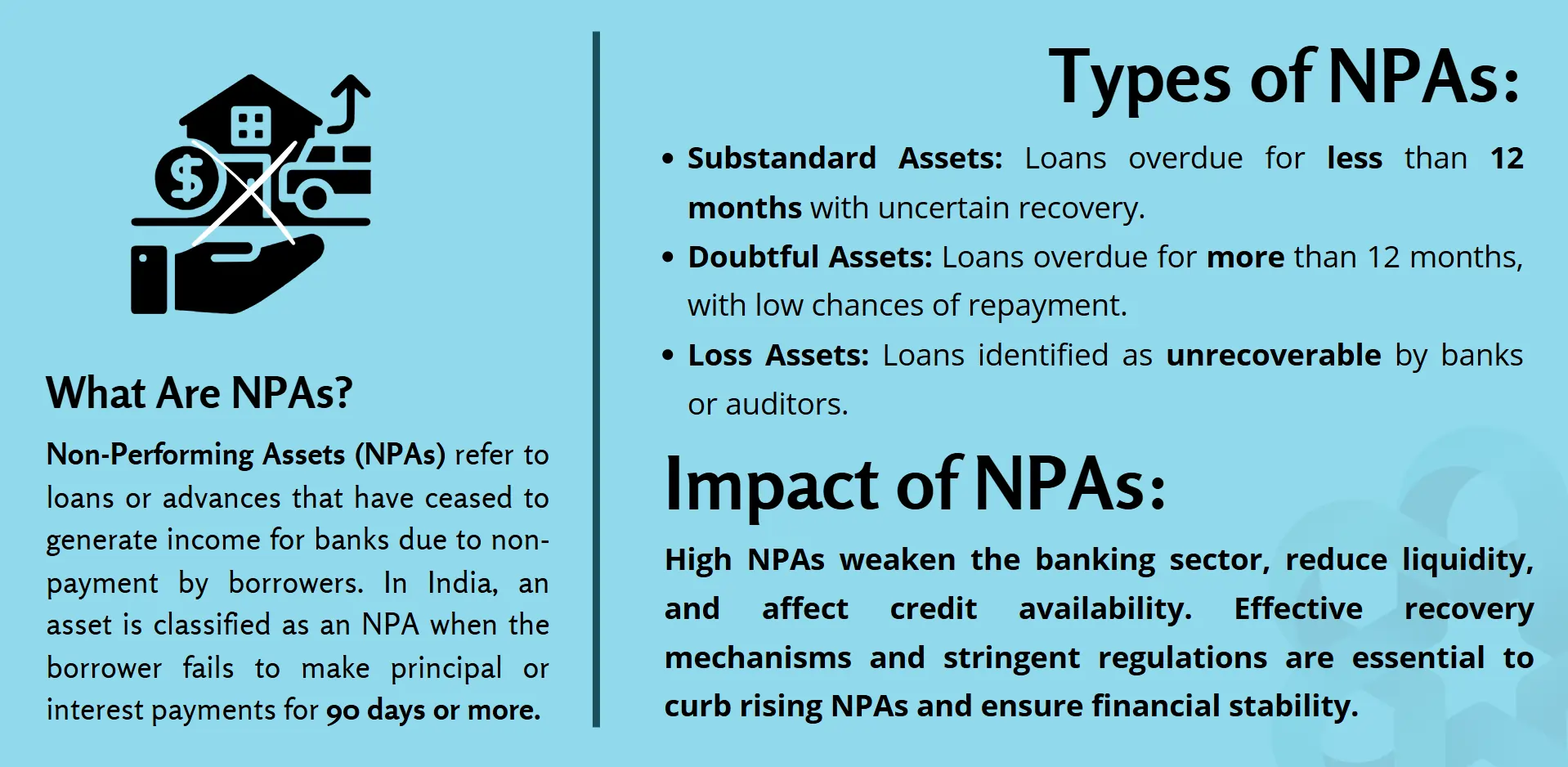

There has been major growth in the Indian banking industry, driven in part by private banks increasing how efficient and digital their services are. At the same time, concerns about non-performing assets, poor management and delay in adopting modern technology continue to affect public sector banks. Though tirelessly addressing the sector with bank mergers and recapitalization, essential improvement can only be made by implementing comprehensive changes.

Digital Finance and the Fin-tech Movement

Digital payments, lending platforms and investment services are all the result of fintech companies’ rise and transformation in financial services. UPI and neo-banking has increased customer access. Nevertheless, not knowing how guidelines will change and worries about cybersecurity challenges in fintech.

Markets for Capital

With improvements such as making it easier for foreigners to invest and boosting company governance, India has grown its capital markets and brought in investors from other countries. Even though the stock market has been bringing in record-breaking profits, investors and regulators must keep an eye out for market swings, illegal trading within the market and financial fraud.

Including Financial Protection

Even though the insurance industry is growing and using digital tools more, many rural residents still find it difficult to get and pay for insurance. Meanwhile, efforts to provide financial access for everyone have advanced, but many rural and small business people are still faced with not enough credit and cash management knowledge.

Laws and the Transportation Industry

Shaping financial policies has largely benefited from the work done by the Reserve Bank of India (RBI) and the Securities and Exchange Board of India (SEBI). Even so, influences from the global economy, inflation and politics need policymakers to use flexible approaches.

Rapid change is happening in India’s financial sector, but extensive reforms are needed to maintain stability, support new developments and include all groups in the financial system.

Important Problems Driving the Sector

Financial reforms and strong growth have yet to solve the main issues facing India’s financial industry. A set of issues like complex regulations, difficulties in banks, gaps in financial inclusion and economic uncertainties call for immediate attention.

Difficulties Regarding Rules and Unclear Policy

India’s financial sector is managed by various organisations like SEBI, IRDAI and mostly by RBI. At the same time, when parts of the financial system are governed by different laws and regulations, progress in innovations is often slowed down and it becomes less efficient for companies to deal with them. Policies that are not in step mostly in technology and finance also negatively affect progress and give new entrances to the difficulties.

Problems within the Public Sector Banking Sector

PSBs are still dealing with a high number of unrecovered loans, challenges managing their organizations and credit management issues. For a number of large PSBs, the issues of low profits, limited autonomy, and politics have not been resolved by attempts to increase capital and join banks. The ability of these banks to remain stable financially depends on better governance structures.

Financial Inclusion and Access to Rural Credit

Even though India has advanced in providing access to financial services, there are still problems for some rural people and small companies to get credit. Due to their uncertainty about risks, traditional banks avoid lending to people with little income, leading many to resort to informal debt solutions. Boosting online finance, helping people become familiar with tech and developing more banks will help reduce this difference.

Way the world’s financial environment affects the country

India’s financial system is affected more and more by changes in world inflation, changing interest rates and regular market swings. Geopolitical stresses and dangers of a global recession can strongly influence investment movements, the performance of companies and the country’s economic health. The sector needs strong policies to protect it from outside disturbances.

Focusing on these important problems helps develop a financial system that supports India’s growth now and in the future.

Need for change in policies

Despite considerable growth in its financial sector, big issues are still found and changes are needed.

- Rebuilding Control and Performance: Public sector banks have not overcome the problems of sluggish operations, large financial losses and poor management. Changes need to be made that improve accountability, reduce political influence and help get loans repaid.

- Digital Transformation: The use of digital finance in India has risen considerably, mainly due to innovations from UPI and new fin-tech companies. Still, using old rules and facing cyber issues is challenging. To increase use of financial technology, policy creators should improve out-dated laws, encourage banks and fin-tech firms to team up and apply better cyber-security solutions.

- Easing Regulations: Because financial markets are controlled by many regulatory organizations, it often becomes complicated to follow the rules and results in slow advancements. Underlying objectives for government regulations will increase the efficiency of businesses. Reducing how much red tape is involved will make it simpler and clearer for banks, fin-tech businesses and investors to function.

- Credit and Banking Services: In spite of efforts to assist them, rural communities and small companies are still having a hard time with credit. Policies affecting loans, helping microfinance institutions and using new banking technologies can solve this problem. Extending financial literacy programs will help individuals and businesses choose their financial actions wisely.

- Sustainable Finance: India is required to comply with the best global financial standards to support the country’s stability. Building a resilient financial system for the future depends on making sustainable policies, improving investment laws and working with other countries.

Bringing these changes into action is important for India’s financial progress and for supporting constant and steady financial growth.

Roadblocks and Reform Implementation

Even though financial sector changes are important for stability and growth, they encounter numerous difficulties during implementation. Problems caused by political resistance, bureaucracy and complicated regulations often result in slowing down important adjustments.

Efforts by Those in Power

Often, politicians and government institutions that gain from how things are don’t want changes in the financial sector. Because public sector banks are guided by political decisions, they often worry about job losses, their finances and government control, so they might resist being privatized. Furthermore, those responsible for setting laws may avoid making big changes that disrupt the current economy.

Technology and cybersecurity

Cutting-edge technology is important for improving India’s financial sector, though it means cyber-security and data privacy risks now exist. Many financial institutions should upgrade their security measures to make it harder for fraudsters and hackers to succeed. But the high cost of new technology and improved security measures is often a big problem that smaller firms face.

Uncertainty about the economy and markets

Changes in the financial world, high inflation and economic hard times can complicate reform efforts. Because unpredictable market changes can influence foreign investment rules, banking policies and fintech, carrying out these policies may be dangerous. For financial reforms to work, it is necessary that economic policies remain stable and confidence among investors is achieved.

Social and Financial Inclusion

Even though there are ongoing attempts to encourage financial inclusion, a major group in India is still unable to access financial services. Changing lending rules and supporting digital banking are ways to help, but both sectors must work together for success.

The Next Steps

It is important for India’s financial system to keep up with broad, far-reaching reforms for stability and to compete well on the global stage. Movement toward simpler rules, improved technology and more access to banking will greatly benefit people.

Improving Banking Management

The public sector banking should emphasize openness and efficiency by introducing strong systems of governance. Private ownership, better credit decision-making and strong loan accountability can improve the financial firmness of weaker banks.

Digital Transformation and Fin-tech Growth

As fintech rapidly progresses in India, it means a better regulatory plan is needed to ensure both progress and safety. Taking steps to streamline licensing for fintech companies, boosting teamwork and improving how cybersecurity is used are ways to speed up adoption and control problems with fraud.

Updating Financial Laws

A consistent and easy method of financial rule-making is needed for a growing financial setting. Less bureaucracy, straightforward rules and using new technology in finance will make things faster and clearer.

Access to financial services and credit

If rural economies and small companies are to become stronger, they need to have access to steady credit options. Widening access to microfinance, building reliable digital platforms for payments and launching specific financial literacy programs will equip the economically disadvantaged to become more involved with India’s finances.

Following the international financial world

India needs to adopt best practices internationally for its financial policies to protect itself from external dangers and boost investor belief in the country. Stronger economic diplomacy, more international financial teamwork and a stable monetary policy can protect the industry from swings in the market while keeping the economy on a growth path.

Following these reforms, India financial sector will be more prepared, welcoming to all and able to succeed as the world’s economy advances.

Conclusion

At the present time, India’s financial sector needs urgent, influential reforms to keep the sector stable and help it grow over time. Although earlier policies have brought benefits, regulatory issues, problems with how banks are run and unmet financial needs for some stop its progress. Crucial tasks for shaping a secure financial ecosystem will be to focus on transparency, adapt faster to digital methods and simplify compliance regulations. Mixing policy innovation, the use of new technology and proper financial practices will steer India toward its economic goals.

When India makes strong changes, it can improve its financial sector to better support companies and individuals’ interests on the global stage. Making only small adjustments is no longer useful; India needs a major reorganization to maintain its position as a leading financial power. By having strong political commitment and close cooperation among financial institutions, the nation can design a modern financial system that provides stability, growth and equality.