|

Key Highlights

- Increasing cybercrimes in India

- Karnataka reported the Highest

- Mule accounts at the centre

- Weak KYC protocols

- Need a coordinated effort

- Focus on Ai-based detection tools

|

This Article analyses the National Crime Records Bureau (NCRB) 2023 report on cybercriminal activity in the state of Karnataka, especially cyber mule accounts, and suggests that banks should be better regulated and that digital fraud protection should be strengthened.According to recent NCRB data and reports from local outlets, Karnataka, particularly Bengaluru, has seen a massive surge in cybercrime, exposing significant blind spots in the state's banking system.

|

Tips for Aspirants

This article fulfils the information requirements of the UPSC and State PSC aspirants by relating the new trends in cybercrime with the basics in governance, digital regulation, and financial integrity, and thus to the major themes in GS Paper 3, ethics, and analysis of current affairs.

|

Relevant Suggestions for UPSC and State PCS Exam

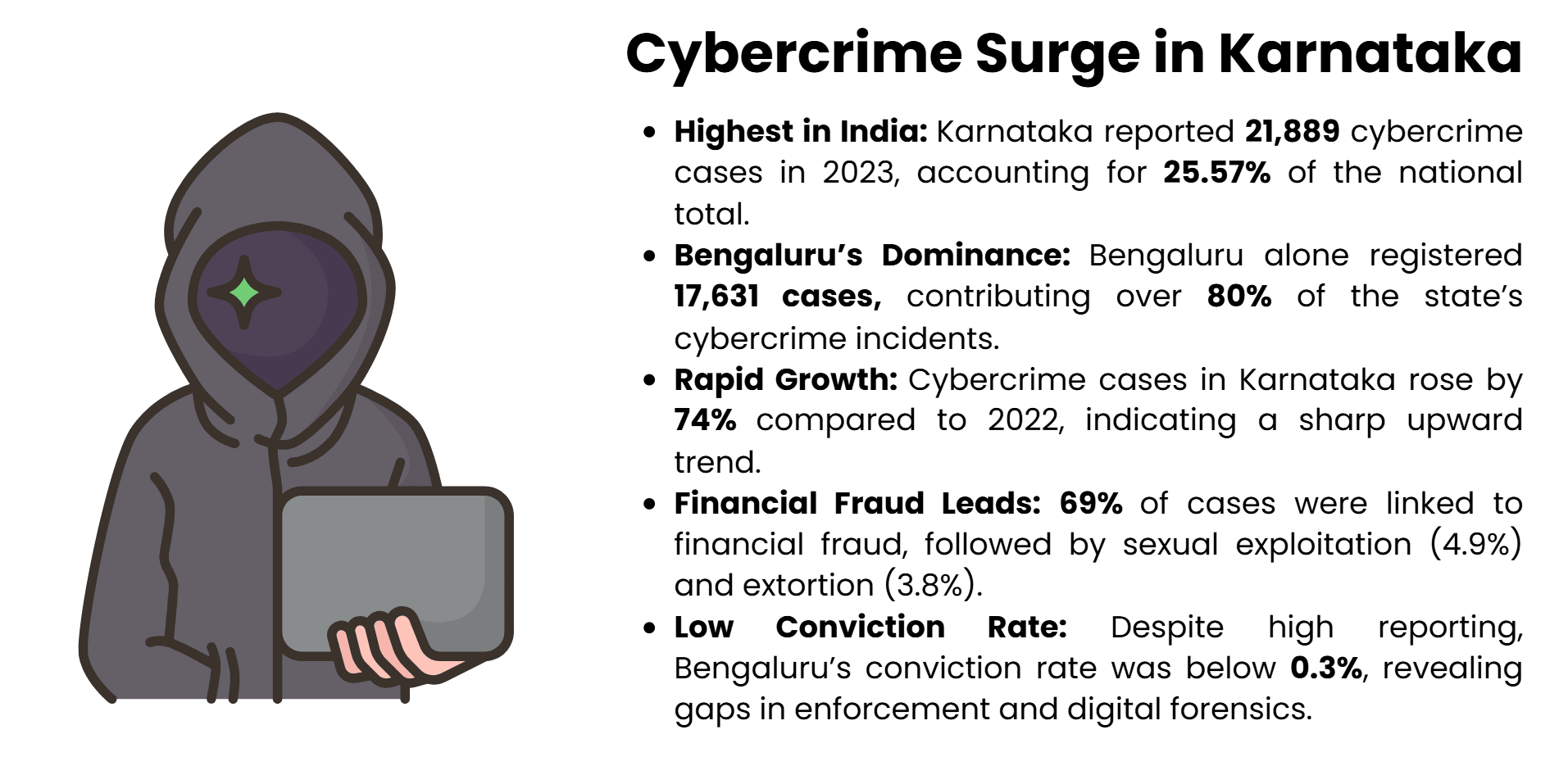

- Karnataka leads the national cybercrime counts, with 25.57 percent of national incidents recorded in 2023, of which over 80 percent alone in the city of Bengaluru.

- Financial fraud stands out as the most common cause of cybercrime, followed by sexual exploitation and extortion; these trends reveal weakness in online financial systems and user knowledge.

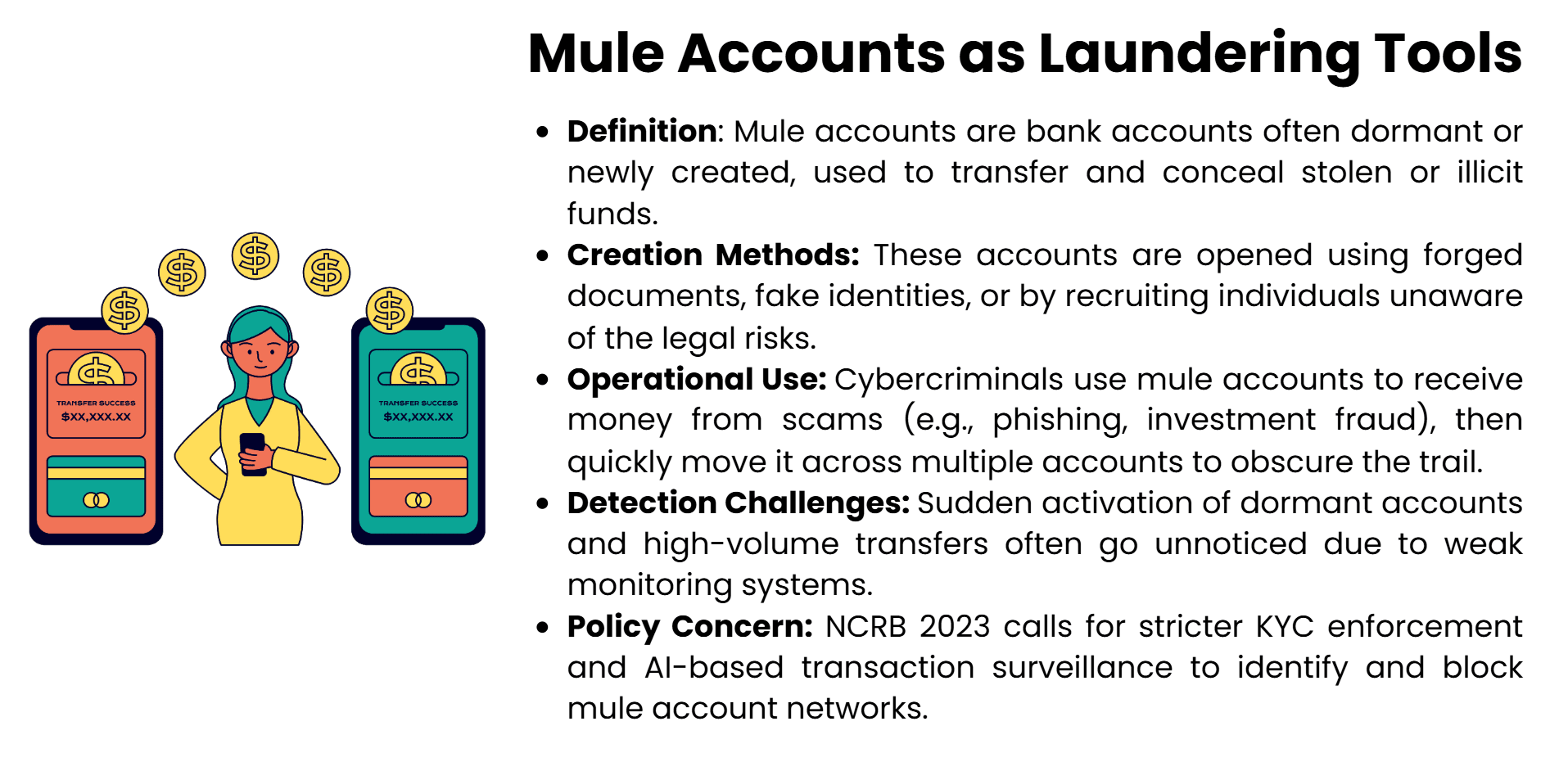

- Mule accounts [which are accounts within a bank that have no activity or which are false accounts] are extremely important in laundering illegally acquired funds and bypassing detection systems.

- With a conviction rate so low at less than 0.3, Bengaluru witnesses problems of severe lack in digital forensic strengths, legislative facilities, and interactions across the enforcing agencies.

- Know Your Customer (KYC) loopholes and weak and poorly recognized identity verification frameworks contribute to the creation of mule accounts, especially in semi-urban and rural bank systems.

- The National Crime Records Bureau suggests using AI-infused fraud detection, biometric authentication, and real-time transaction monitoring as policies to support banking oversight systems.

- A coordinated, efficient response to cyber threats cannot be achieved without effective collaboration among agencies and consolidation of databases on cybercrime.

- Raising awareness of what money mules represent and improving financial literacy represent crucial steps to discouraging enrolment in money-mule networks and encouraging sound cyber security practices.

|

According to the 2023 report by the National Crime Records Bureau (NCRB), the overall trend in cybercrime in India is negatively increasing, with a central point in Karnataka. With the following online relationships growing into sectors, the state is being severely affected by the technologically enhanced fraud in finance, as well as identity and online deception. Amongst the most disturbing pieces of news is the fact that there has been the creation, and still continues to be created, of what are known as mule accounts(bank accounts that are dormant or accounts that were only opened very recently under false identities and false addresses), which are being utilized in order to launder the proceeds of crime. These accounts use the system as a way of allowing cybercriminals to cover the tracks of transactions and evade detection, which is a big threat to businesses, and the police. The report also reveals institutional vulnerabilities in the policing of banking, particularly in relation to the inspection of Know Your Customer (KYC) and the real-time monitoring of possibly suspect account activity. The Report calls for increased vigilance and inter-agency co-operation to counter the misuse of digital infrastructure.

Rising cybercrime in Karnataka

To this effect, this article examines the findings by NCRB, explores how the mule accounts actually work, challenges the regulatory weaknesses in the banking industry, and recommends policy options to strengthen cyber governance. This way, the article puts into perspective the cybercrime trend in Karnataka against the backdrop of national and international trends in cyberspace, thus explaining the changing dynamic between online finance and crime.

NCRB Report 2023: Cybercrime Data

The 2023 report of NCRB outlines a sharp increase in online crimes in the state of Karnataka, which makes the state a staggering hub of cyberspace weaknesses and fraudulent activities across the country.

National Standing in Cybercrime

The 2023 Crime in India report, released by NCRB, revealed Karnataka contributed 25.57 % of all cases of cybercrime in the nation, summing to 21,889 casesand highest number across country. It is not the only upsurge since 2022, with 12,556 cases being reported. The surge is indicative not just of rising digital penetration but of increased scope of cybercriminal activity. Karnataka outpaced all the other states in the region like Telangana (18236 cases), and Uttar Pradesh (10794 cases), implying that there is a cluster of cyber threats in southern India.

Bengaluru

Bengaluru alone reported 17,631 cases, 80 percent of the total Karnataka cases, and more than 51.9 percent of the total of reported cases in 19 metropolitan cities. The city had the highest rate of cybercrime at 207.4 cases per lakh population, more than seven times higher than the national rate. The overwhelming increase to almost 18,000 cases by 2023, compared to 6,423 in 2021, indicates systemic exploitation of urban digital infrastructure and user knowledge. Financial fraud was identified as the most common motive of these offences (69%), followed by sexual exploitation (4.9%)and extortion (3.8%).

Gap in Detection and Conviction

Although there are growing cases reported, the cybercrime detection rate is low at 18% and conviction rates are non-existent in Karnataka. By 2023, just 44 convictions had been recorded in the state, of which 11 were from the previous year, alongside 60aquittals. The conviction rate in Bengaluru stood at less than 0.3%, showing that there was a dire gap between the reporting and judicial disposal. Such a mismatch can be attributed to difficulties in digital forensics, inter-agency & coordination issues, and the changing face of cybercriminals.

New Directions and Implications

The data given by the NCRB also draws light to the introduction of mule accounts (bank accounts without a real name, or even those with questionably real and possible names), opened, left inactive, and used to launder stolen money. These descriptions make it more difficult to detect and trace activity, which has led to higher scrutiny of banks and real-time tracking. The findings presented in the report highlight the urgency of cyber security education efforts, fraud detection through AI, and extensive policy change to mitigate the changing threat landscape.

Mule Accounts

In the report released by NCRB, mule accounts have been listed as a central facilitator of cybercrime in the Indian states. These are defunct or forged accounts that are used to launder away illegal online revenues.

What are Mule Accounts, and what is their functional role?

Mule accounts refer to bank accounts used by felonies to receive, hold, or withdraw money collected illicitly without detection. Creating these accounts does not usually require any legitimate documents or authentic identities, or distorted location data. Often, these accounts remain dormant until they are used to complete a particular fraudulent transaction.

- Their main aim is to spin the identity of the origin and final destination of stolen money, and to make it difficult to carry out an investigation to trace the financial trail.

- • The NCRB report sees mule accounts as an increasingly acute problem, especially in some states like Karnataka, where digital fraud is rampant.

Modus Operandi

Criminals often recruit people to open bank accounts, usually not knowing it fully, to initialize payments at comparatively small fees.

- The recruited, characterized as money mules, are typically students, unemployed young adults or otherwise vulnerable people unaware of the legal implications involved.

- In another strategy, attackers use artificial identities created when data is stolen or falsified documentation to create an account in a distant location.

- These accounts capture proceeds of a phishing scheme, investment fraud, or ransomware payments, after they become functional.

- The embezzled savings are immediately banked out or repurposed to peripheral mule accounts, thus creating a complex system of transactions that sap the effectiveness of law-enforcement efforts.

|

Know Your Customer (KYC) principle

|

|

The Know Your Customer (KYC) principle is a pillar regulation in the banking system of India, and it aims to determine the identity, location, and money situation of customers. KYC, a requirement of the Reserve Bank of India (RBI), aims at deterring financial crimes like money laundering, identity theft, and misuse of banking services by illegal operations. The process includes gathering and authenticating documents like Aadhaar, PAN, voter ID, and residential proof under given conditions, as well as the introduction of biometric records.

KYC has two main steps to follow, which are Customer Identification and Customer Due Diligence. This bifurcation is supported by the fact that financial institutions are required to revise information more often, and to do enhanced due diligence on high-risk accounts at least once annually. The introduction of e-KYC systems and Aadhaar-based authentication has enabled easier registration because of its application in isolated and underserved areas. However, biological identities and the ability to trace dormant accounts remain a challenge.

|

Bank Control and Shortfall in Regulations

The NCRB requirement emphasizes the need to intensify examination of the identification and monitoring of mule accounts by financial institutions.

- Despite the existence of reasonable efforts in relation to the existence of the Know Your Customer (KYC), there are still gaps in the identification of identities and the tracking of the movements of inactive accounts.

- Many banks do not have complex systems that can isolate suspicious behaviour, like sudden deposits into dormant accounts or large deposits into new accounts.

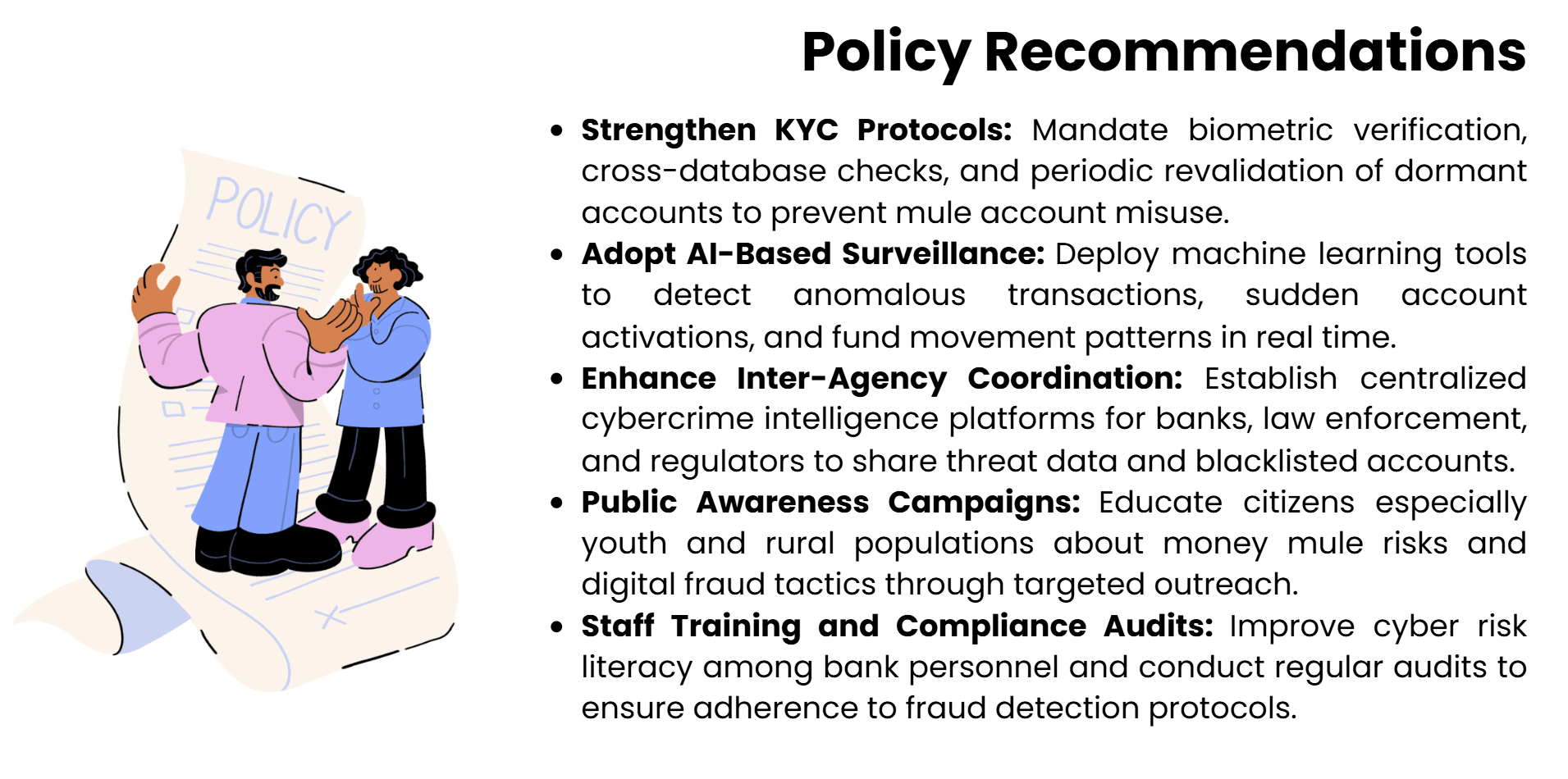

- The report recommends that, to prevent such exploitation, artificial-intelligence-based fraud detection technologies and the hardening of inter-agency data exchanges should be incorporated.

Implications for Cybercrime Prevention

The prevalence of the mule accounts comes with massive implications. In addition to supporting economic malfeasance, these accounts destroy the trust that people have in online banking frameworks. Reducing this risk requires a complex approach that includes strengthening KYC protocols, educating people about the dangers of money mules, and increasing co-operation between banks and fiscal authorities on the one hand, and law enforcement agencies on the other.

The Role of the Banking sector and Gaps in Sector regulation

The NCRB report proves the paramount importance of the banking sector's effort to reduce and eliminate cybercrime, but also demonstrates a major regulatory fault that helps mule accounts and other financial scams to be developed.

Inadequate Monitoring

Despite the introduction of Know Your Customer (KYC) principles, the report shows that banks often are unable to detect suspicious trends in account usage. Cybercriminals use the accounts as a means to launder illegal funds, making them a crucial component of an online fraud ecosystem. The fact that many banking systems do not track transactions and their behavioural indicators in real-time, as well as the ineffective preventive functionality, leads to underperforming detection and a slow response.

KYC compliance and identity verification

Systemic gaps in terms of overall identity verification in identity-defining procedures undermine their effectiveness. To bypass standards,scammers use a mix of genuine and fake IDs. Banks that undertake the effort to authenticate their customers in rural and semi-urban areas find it harder, as the documents may not be of standard quality. So the NCRB report suggests a holistic approach to KYC practices, supporting the use of biometric identification, cross-database authentication, and interrelation with national identification systems to hinder illegal usage of banking infrastructure.

Fragmentation of Regulation

One of the major barriers to successful cybercrime prevention is the disjointed regulatory environment. There is limited coordination between various agencies, such as the Reserve Bank of India (RBI) and the Ministry of Home Affairs, and state-level cybercrime units. This isolated method negatively affects direct sharing of information and collective response mechanisms. The NCRB also confirms the importance of inter-agency partnerships, central scams databases, and uniform reporting measures in ensuring prompt response to mule account systems and online monetary violations.

Strengthening Oversight Recommendations

To address such gaps, the report suggests that AI-based fraud detectors that have the capacity to raise a flag on anomalies in transaction behaviour should be adopted. Moreover, it requires regular auditing of dead accounts, the awareness of the personnel about managing cyber-risks, and the education of the community about the process of hiring money mules. Improving internal adherence structures and building a culture of active vigilance in banking entities will be critical in protecting digital financial environments.

Enhancing KYC and Account Verification Process

Implementing a complete redesign of the Know Your Customer (KYC) mechanisms is a historic suggestion.

- Its report recommends that banks take up biometric verification, cross-check with Aadhaar and PAN databases, and undertake regular re-check of inactive accounts.

- The creation of mule accounts can be pre-empted by greater scrutiny of new accounts that have little to no history of transactions, or whose addresses are unverifiable.

- Regulatory authorities need to apply tighter compliance audits and punishments to institutions that are not successful in catching fraudulent onboarding practices.

|

AI-based Fraud Detection Systems

|

|

Ai-driven fraud detection software is an innovative system related to financial security in the Indian banking industry. These systems will use machine learning computations to inspect great amounts of transactional information within its stride and identify designs of behaviour that are not linked to persist regular customer behaviour. Using previous data, AI can detect abnormal events, like the sudden increase in fund transfers, unusual log-in locations, or quick currency transfers in two or more accounts, usually pointing to mule’s activities or phish-based fraud.

Unlike deterministic systems, AI systems are updated in response to new attacks and can make inroads into advanced cybercriminal schemes. Banks combine these systems with customer profiling, geo-location tracking, and fingerprints of the device to make them more accurate. Upon the identification of suspicious activity, they generate alerts to be reviewed by a human or automatically respond with potential actions like blocking transactions or launching a verification process.

|

Inter-Agency Co-ordination and Central Reporting

Cybercrime response, as currently organized in individual pieces by banking regulators, cybercrime cells, and state police, requires a unified structure.

- NCRB suggests creating a more central cybercrime intelligence repository that can be accessed by banks, police, and regulators. This would enable the prompt exchange of threat indicators, black-listed accounts, and new typologies of fraud.

- The experience of Karnataka highlights why a state-level cybercrime coordination task force is important to simplify investigations and policy enactment.

Community awareness and preparedness

- There are a lot of people who become money mules because they are not aware of what money mules are.

- Specific campaigns, especially in universities, employment sites, and rural banking facilities, should be used to educate citizens with regard to the legal implications of being involved in a mule account.

- At the same time, banks will need to invest in employee education to identify red flags and react when suspicious activities are in place.

- Detection and prevention of cybercrime should be integrated into the financial literacy initiative and online onboarding measures.

Conclusion

The report on crime statistics provided by the National Crime Records Bureau (NCRB) 2023 gives a clear insight into the changing world of cybercrime, both in terms of the level of digital crime and the flaws in the system that allow it to happen. Formation of mule accounts, eased with poor identity checks and a lack of proper banking regulation, is strong evidence of the ineffectiveness of institutional change. Although the banking sector is vested in the core of financial integrity, its existing regulations (symbols of regulatory capacity) have limited responsiveness to combat complex cybercrimes. The multidimensional strategy when it comes to preventing cybercrime is evident in the report, specifically the focus on AI-driven surveillance, inter-agency coordination, and public awareness. The case of Karnataka is an example of a microbiotic sample of national issues in digital governance, which requires active policy development and strong infrastructure measures. These concerns are not about imposing a ban but protecting the shared belief among people in electronic systems. With cybercrime undermining geographic and institutional jurisdictions, a coordinated, technology-based, and ethically-based response is necessary to long-term security.