|

Key Highlights

- Fall in Inflation

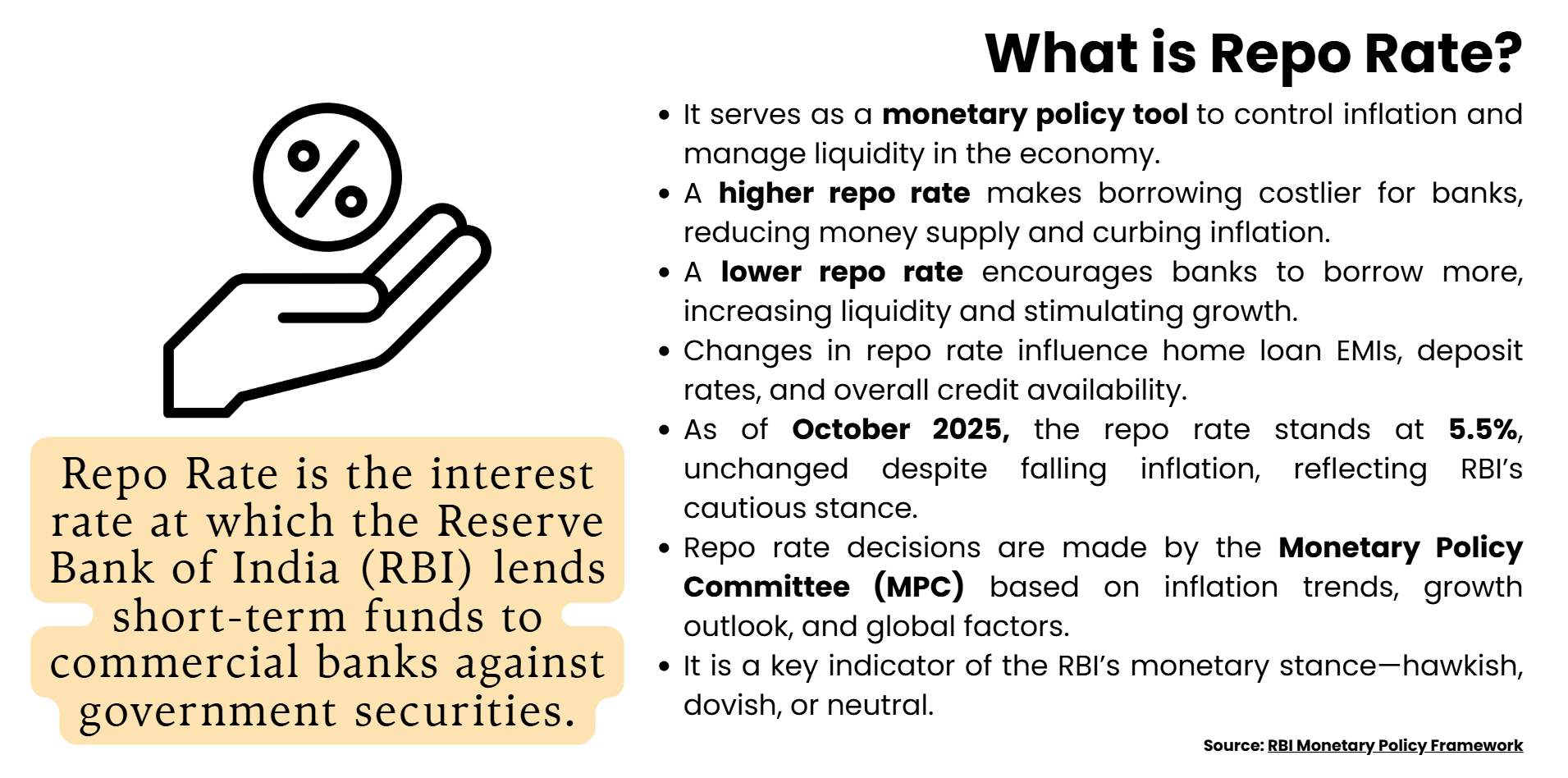

- Hold on Repo rate at 5.5% by RBI

- Revised GDP Forecast at 6.8% for FY 26

- Regulatory easing

- Credit expansion for NBFC’s and Banks

- Balanced Approach: stability with stimulus

|

The interest rates in the policy by the RBI are stable and RBI prefers not to accelerate growth but rather encourage expansion with banking laws and sectoral reforms.The Reserve Bank of India (RBI) released its Monetary Policy Report (October 2025) following the 57th meeting of the Monetary Policy Committee held from September 29 to October 1, 2025. RBI has kept the repo rate unchanged at 5.50% with a neutral stance.

|

Tips for Aspirants

The article can support the aspirants of the UPSC and State PSC examinations by clarifying the connection between the monetary policy of the RBI and the spheres of economic policy, financial prudency, and inclusive development, which are the focus of the GS Paper III examination and the current affairs.

|

Relevant Suggestions for UPSC and State PCS Exam

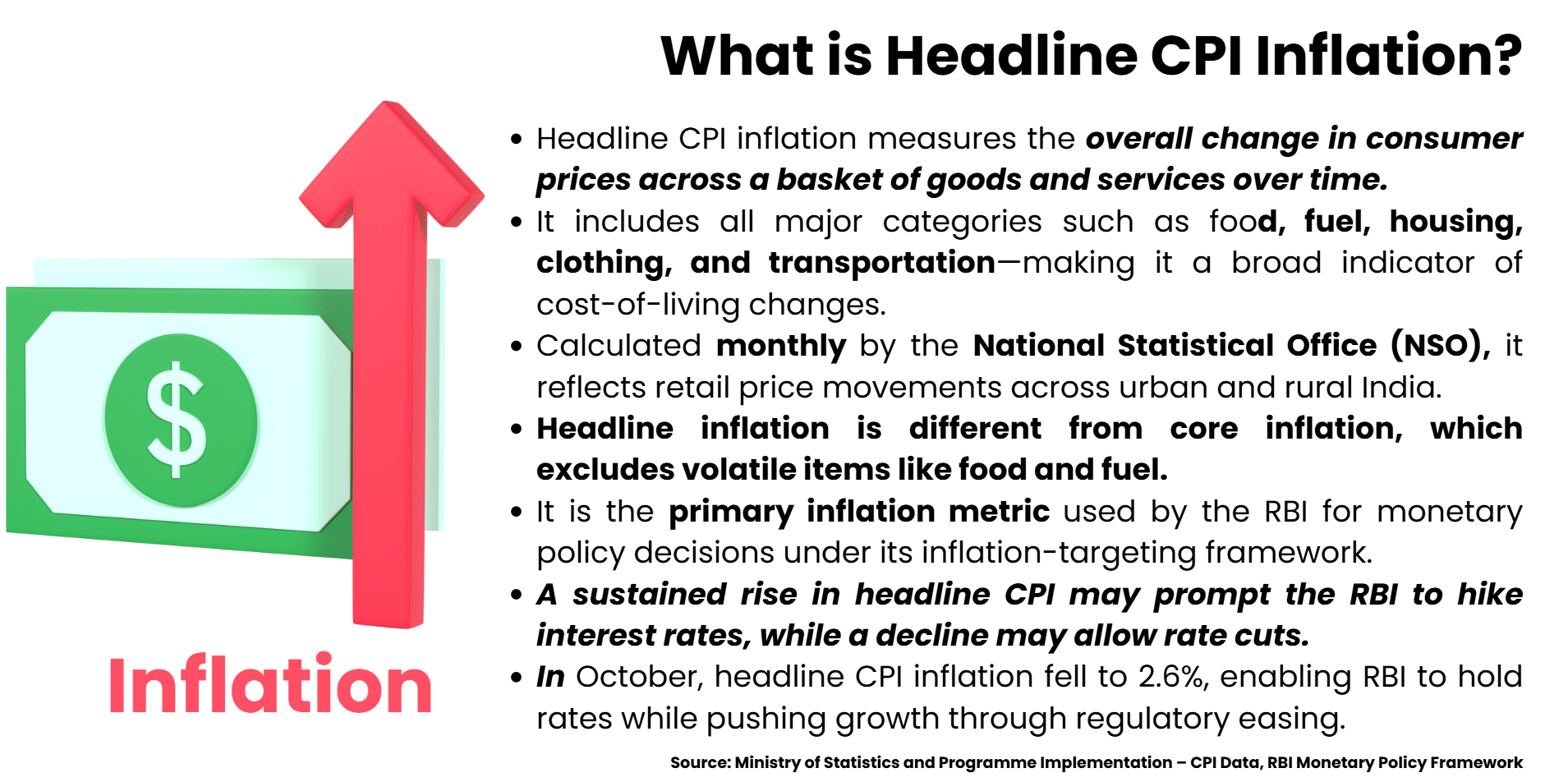

- The RBI has held the repo rate at 5.5%, despite a CPI-based inflation dropping to a 2.6% level, thus indicative of a prudent, strategic, and flexible approach.

- The GDP growth projection is also revised to 6.8% in FY26 as a result of strong consumption, investment, and services industries.

- The RBI has alternatively resorted to structural reforms, relaxation of norms in loans, NBFCs, foreign exchange, as a form of growth fomentation other than further cutting rates.

- The RBI has allowed banks and NBFCs to grow credit by relaxing provisioning and capital requirements, making the banking sector one of the drivers of growth.

- RBI has had a data-dependent strategy where it balances between inflation control and supporting growth, so it has remained neutral.

- The simulative impact of previous declines in rates is still in effect, and so the RBI should then be cautious when initiating further reduction actions.

- RBI has maintained a rate cut powder dry to address any imminent vulnerability in the future.

- There has been a diversion to the long-term structural reforms stimulus rather than monetary accommodation.

|

Key Highlights of RBI Monetary Policy 2025: Growth Without Rate Cut

The October 2025 monetary policy review of the Reserve Bank of India is currently a decisive point in the changing approach taken by the central bank to bring a balance between macroeconomic stability and the need to grow. Although the headline inflation of consumer price index (CPI) fell to 2.6%, the lowest in eight years, the RBI preferred to keep the headline unchanged, at 5.5%, indicating a well calculated move and not a retaliatory measure. Such a decision shows that the institution has taken an astute insight into the economic course of India, and the strategy of monetary accommodation is currently being adopted, but through regulatory relaxation and reforms in various sectors.This policy position reflects the optimism of the RBI in the growth momentum in India, where statistics on GDP have been adjusted to reach 6.8% in FY26. The central bank wants to empower financial institutions as instruments of inclusive growth by easing the requirements on credit growth, efforts to finance infrastructural developments, and the management of foreign exchange. This was actually a strategic decision of keeping the interest rate powder dry and using the regulatory levers to work, as opposed to the monetary/structural facilitation of this effect.

This multidimensional policy framework is discussed in the article, with its implications on the banking sector dynamics, inflation targeting and, the long-term economic resilience examined.

Status Quo: Repo-Rate

In October 2025, the Reserve Bank of India (RBI) decided not to reduce the repo rate, so it decided to adopt a purposeful pause against the background of receding inflationary trends and a stable economic growth rate. This is a risky step that nevertheless indicates the strategic flexibility required in coping with changing macroeconomic circumstances.

Inflation and policy prudence

Headline Consumer Price Index (CPI) inflation decreased dramatically, it was 2.1% in August 2025, triggering a decline in the forecast of the full-year rate to 2.6 percent, the lowest since 2017. Such temperance owes down to a pleasant monsoon as well as to better food supply networks, as well as rationalised GST rates. Even though this was a positive inflationary climate, the RBI refrained from cutting rates.

Cumulative Easing and Transmission Lag

Earlier in 2025, the RBI released a cumulative decrease in the repo rate by 100 basis points over three tranches: February, April, and June. The aim of the cuts was to make credit more affordable and boost the demand. However, the central bank observed that transmission of them to the broader financial system is yet to be handed over fully. The RBI also keeps the rate constant to take time before banks can change the lending rates, and also allows the economy to absorb the previous stimulus.

Strategic Flexibility

The Monetary Policy Committee (MPC) has voted unanimously to maintain a neutral position, in that its strategy is data-dependent. This position allows the RBI to be responsive to future events, such as external shocks, as well as fiscal policies and international monetary trends. The choice is also part of prudence in the face of world uncertainties in the form of increased U.S. tariffs, currency risk, and geopolitical risk, which may affect inflation and capital flows.

|

Monetary Policy Committee (MPC)

The Monetary Policy Committee (MPC) is a statutory agency under Section 45ZB of the Reserve Bank of India Act, 1934, which stipulates the setting of the benchmark interest rate in the pursuit of the inflation target. In 2016, a new structure of a transparent and accountable monetary policy in India was formalised, which is consistent with global best practice.

|

- The committee is made up of six members, three of them nominated by the RBI, and three independent members, chosen by the Government of India to serve for a period of four years.

- The MPC meets a minimum of 4 times in a year. The vote is carried by majority; each member has one vote, and the Governor has a casting vote, in case of a tie.

- The committee has the primary role of keeping prices stable and aiding in economic growth with a medium-term inflation rate of 4 %2%.

- The discussions and decisions of the MPC are made public so as to encourage transparency, and its decisions have a direct impact on repo rate, liquidity environment, and movement of credit in the economy.

|

Outlook and Prospect of growth

The GDP growth of India in FY26 has changed to a higher level than the earlier 6.8% and this is backed by the strong performance of the Indian sector in the field of private consumption, investment, and services. Such a positive perception reduces the urgency to rate cut downs. However, RBI has indicated that there is still room to fuel more easing in the future in case growth is poor or inflation is underestimated.

The decision to maintain the rates constant proves a measured strategy by balancing between inflation and growth by the RBI. The move is indicative of confidence in the economic fundamentals in India and the maintenance of monetary tools against events.

Growth Optimism

This intended transition to a protocol of regulatory facilitation, as reflected in the Reserve Bank of India’s monetary policy statement in October 2025, owes much to a reassessment of the advancement of the Indian economy and macroeconomic solidity after a decade of concerted efforts of stimulus measures based on rates alone.

The growth forecast

RBI revised its projection of the gross domestic product growth of India in the fiscal year 2026by 6.8%, which RBI attributes to strong growth in private consumption, improvement in rural demand, and continuing favourable sectors of services and manufacturing. The positive monsoon performance, the stable prices of commodities, and increased investment in capital formation in both the private and government sectors are factors that one can attribute to this revision. Extreme confidence as to the momentum that the economy is currently achieving by the central bank has allowed it to apply policy focus not upon traditional policy of rate reduction but upon institutional facilitators of credit and investment.

Regulatory Measures to increase credit

The bank avoided a reduction in repo rates, but it came up with specific regulatory relaxations aimed at increasing liquidity and credit flow. Among the major provisions are the relaxation of norms on lending on shares, widening refinancing windows on infrastructural projects, and simplification of foreign-exchange management to exporters. These projects will enable banks and non-banking financial (NBFC) institutions to efficiently distribute credit, especially to microsmall and medium enterprise (MSME), housing, and green-energy businesses.

Enhancement of the Financial Institutions

The policy also highlights the need to strengthen the institutions of the banking sector. As a supplement to changes in capital adequacy requirements affecting well-rated NBFCs, the RBI has given extra leeway in provisioning priority sector lending. The aim of these reforms is to ease the compliance burden whilst maintaining prudential protection. Through the increased flexibility of operations that it provides to financial institutions, the RBI aims at unearthing credit growth without compromising system stability.

A Stimulus Shift towards Structure

Such aneasing of the regulations marks the shift in the cyclical stimulus towards structural enhancement. The RBI not only provides stimulus packages through interest-rate manoeuvres, but also involves its repertoire of regulatory instruments to deal with industry-specific bottlenecks and raise credit availability. The strategy indicates a comprehensive insight into the Indian economic needs, where lasting long-term economic development not only depends on access to cheaper capital resources, but also on effective financial intermediation and equitable access to credit.

Strategic Shift

Reserve Bank of India's changes in monetary policy in October of the year 2025 are a positive sign of strategic realignment that the banking sector has been treated as a lever of growth, and not just through changing the interest rates.

Re-aligning Bank Transmitted Channels

The move by the Reserve Bank of India to keep the repo rate unchanged at 5.5% and implement regulatory reforms is a reverse strategy of direct monetary stimulus to enable financial institutions to promote credit growth. Recognising its lag in transferring previous rate cuts, the central bank has decided to support the capacities of banks and non-banking financial companies (NBFCs) to lead in transferring the liquidity to the productive sectors.

Relaxing norms for targeted Lending

Some of the main actions taken are relaxed provisions on loans backed by stocks, simplified procedures on external commercial loans (ECBs), and an increase in refinancing infrastructure and green-energy programs. The steps will serve to minimize friction in the credit delivery, especially in the sectors that have high growth multipliers. The Reserve Bank of India has also simplified the foreign-exchange regulation of the exporters to enhance liquidity and competitiveness in the international markets.

Building the power of NBFCs and Cooperative Banks

The policy gives NBFCs and cooperative banks increased operational flexibility, which is a significant driver of last-mile financial inclusion. The Reserve Bank of India aims to minimize the compliance costs without impairing the systemic safety, by aiding capital adequacy standards on well-rated organisations, and also allowing banks to provide distributions to priority sector loans. These reforms are expected to expand credit access among other micro, small, and medium enterprises (MSMEs), rural borrowers, and informal sector members.

|

NBFC’s

|

|

NBFCs consist of financial institutions offering banking-type services, but they are not fully licensed as banks. With a role regulated by the Reserve Bank of India Act, 1934, NBFCs contribute significantly to the overall Indian banking sector in an environment that is formal in giving credit to underserved sectors, including micro enterprises, small enterprises, and rural lending, as well as informal sectors. Whereas banks receive demand deposits, NBFCs are not allowed to do so but also operate by making loans and advances, asset financing, leasing, and investment in marketable securities.

NBFCs are differentiated into specific categories depending on the main flows of operation, i.e., Investment and Credit Companies (ICCs), Infrastructure Finance Companies (IFCs), and Microfinance Institutions (MFIs). The easing and go-to-market strengths of these entities make them indispensable to financial inclusion, especially in those areas where formal penetration of the banks is yet to be adopted.

Over the last few years, the Reserve Bank of India has raised the standards of regulatory review of NBFCs to protect financial stability. In 2022, the regulator unveiled a scale-based system of regulation wherein the prudential regimes are scaled up or down depending on the size and risk obliteration of the NBFC, and hence contributing greater transparency and resilience.

|

Banking Sector as an engine of Structural Growth

This policy shift provides important insight into how the Reserve Bank of India has recognized that the banking sector is not only disciplined to be a transmission belt of monetary policy, but importantly to be a wheel of structural, inclusive growth. Using the tools of regulation, the central bank will provide a kick start to the investment and consumption without affecting financial stability. This mode is an indicator of a wider conception of the economic architecture of India, whereby high financial intermediation is needed to sustain long-term economic growth.

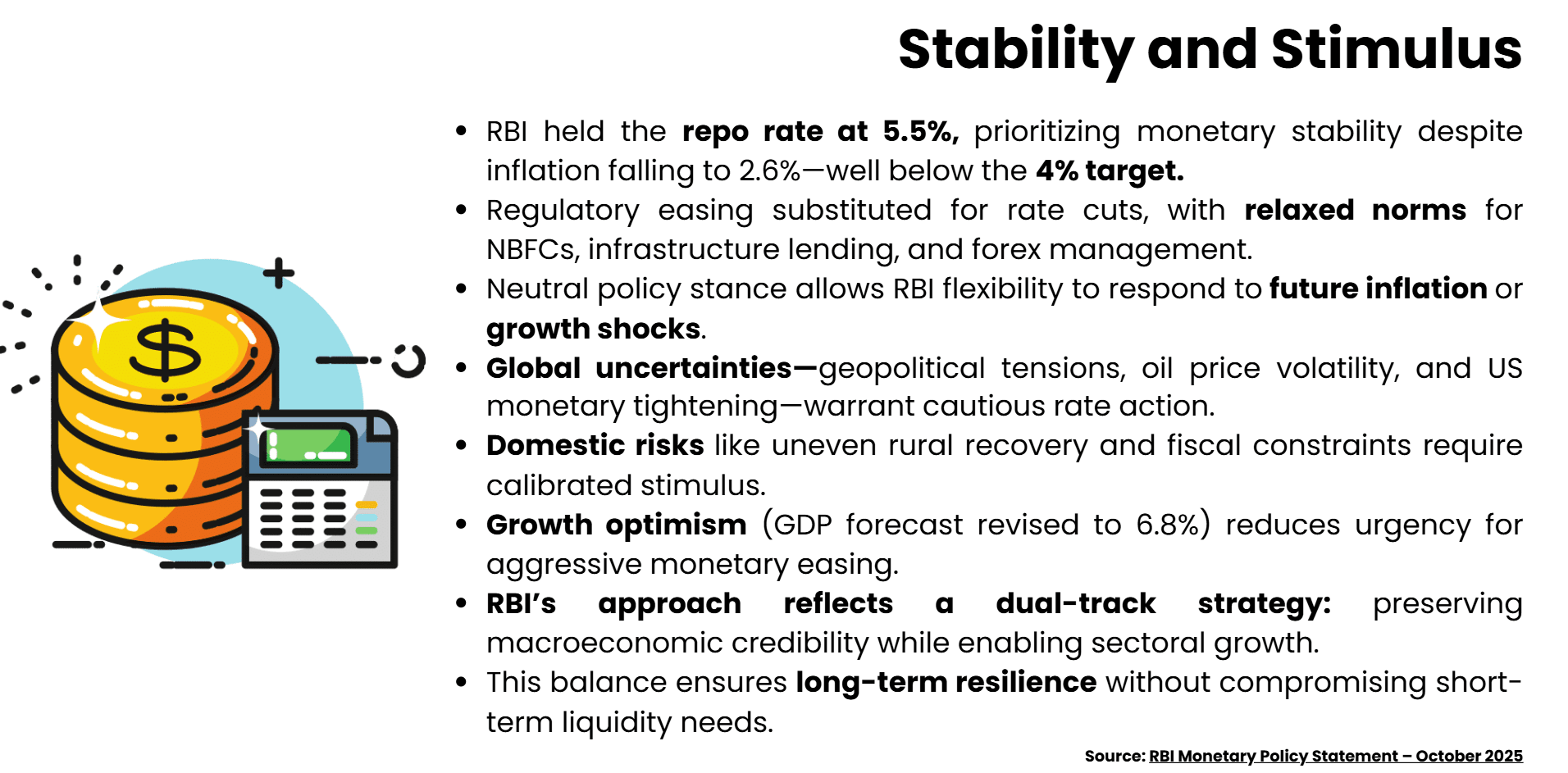

Striking a Balance: Stability and Stimulus

- Maintaining Monetary Credibility: The RBI reaffirms monetary discipline by maintaining the repo rate unchanged at 5.5percent even as the inflation rate declined. Headline CPI Inflation dropped to 2.6%, far below a medium-term target of 4%. The central bank, however, did not act by directly lowering the rate, which denotes that the credibility of the policies and anchoring the inflation is most important in the supreme position.

- Regulatory Easing: Rather than the traditional rate-based stimulus, the RBI used engineering tools to enhance economic growth. There were loans to structures to be secured by relaxation of norms, refinancing increased facilities to infrastructure projects, and ease of foreign exchange rules to exporters. The goals of these interventions are to enhance easier access to credit and liquidity without being fiscally irresponsible.

- External and Domestic Risk Management: This neutral position of the RBI is also an indication of sensitivity to global and domestic uncertainty. Enhanced geopolitical tensions, unstable oil prices, and stringency by advanced economies pose threats to the Indian external sector. Domestically, there is slow distribution of recovery in rural areas and fiscal strain, which are better offset with facility and delicacy. In keeping its interest-rate powder dry, RBI maintains the option of responding to shocks coupled with the ability to maintain the momentum.

- Belief in Growth Fundamentals: The GDP forecast of India has been revised to 6.8 percent in FY26 because of the resilient consumption, investment, and services. This optimistic outlook decreases the hastening of aggressive monetary easing. RBI decided to haltthe rate increasewhile enabling credit creation. Itreflects a long-run stability over short-run stimulus.

Conclusion

Monetary policy by the Reserve Bank of India in October 2025 is a fine-tuned multidimensional macroeconomic governing strategy. Maintaining the repo rate at 5.5% during a substantial fall in inflation implies no more than a clear show of intent by the RBI to hold the monetary stability, but remain flexible in case of future easing.At the same time, the introduction of regulatory reforms to improve the flow of credit, the reinforced position of financial institutions, and the investment in the various sectors could be considered an indicator of a transition to the strategic direction towards structural inducement.This two-pronged framework, reconciliation between restraint in the interest rate policy and active regulatory facilitation, represents confidence of the central bank in the potential growth characteristics in India and its readiness to respond to risks as and when they arise. In its turn, the policy denotes that monetary accommodation can change into anticipatory governance, moving the banking sector into the forefront of inclusive and resilient economic growth.