|

Key highlights

- import dependence on crude oil

- declining home production

- increase in automobile and industrial demand

- diversification of sources as a priority

- Strategic Petroleum Reserves (SPR) expansion

|

The fiscal year 2026 is set to push the dependence of India on the importation of crude oil towards the growing number of demands, as well as loss in domestic production which will deepen the apprehensions about the energy security and economic strengths. "Beyond the Barrel" refers to India's energy security strategy moving beyond its heavy dependence on crude oil imports toward diversification and cleaner energy.

|

Tips for Aspirants

The current analysis will provide insights that are vital in the analysis of the energy security of India, fiscal policy, and strategic planning as some of the major themes in the UPSC CSE and State PSC examinations, especially in the economic, governance, and current affairs sections.

|

|

Relevant Suggestions for UPSC and State PCS Exam

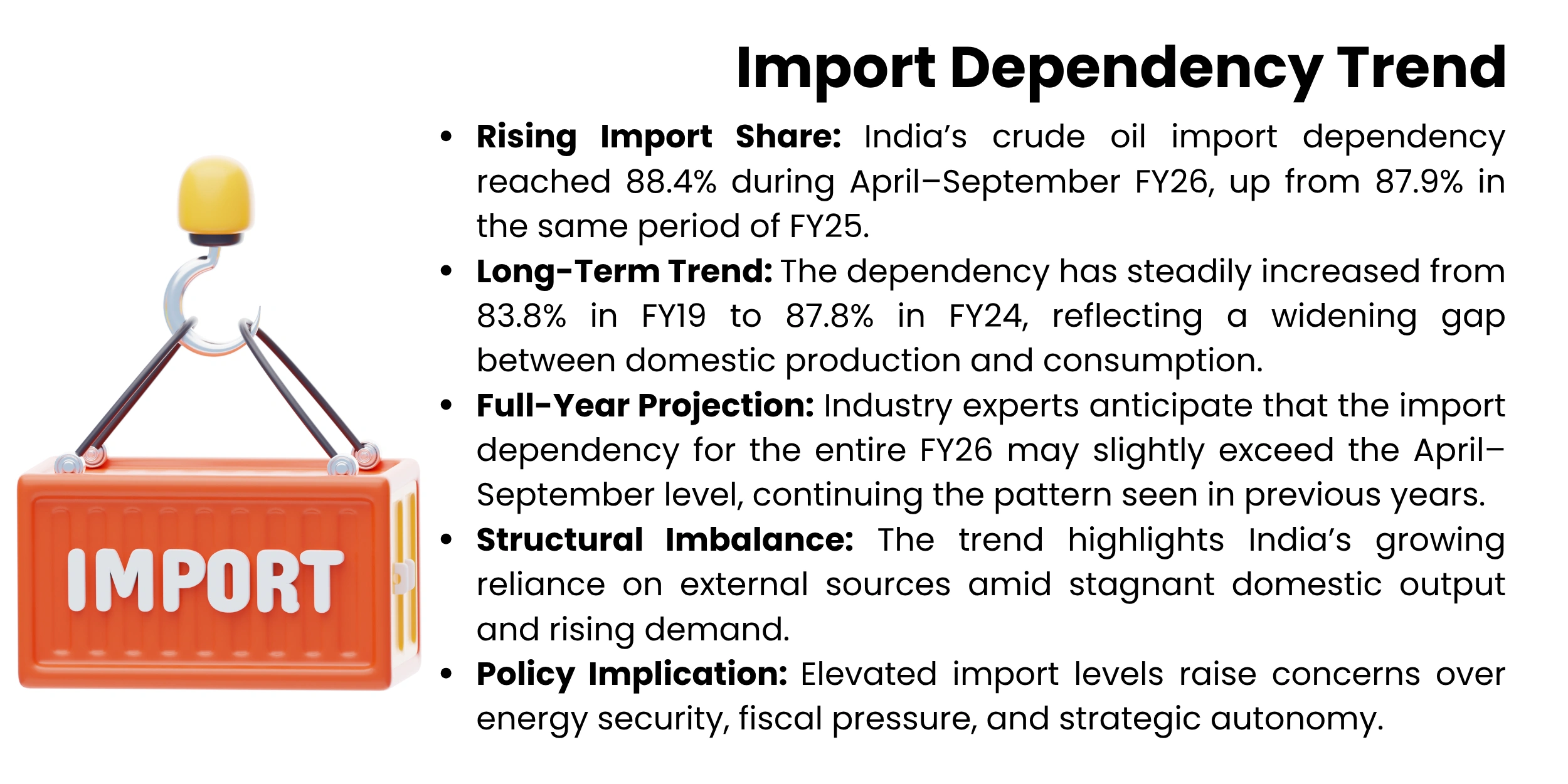

- Import Dependency Trend: The import dependence in crude oil rose to 88.4% which occurred in April to September FY26, which follows a trend of upward exposure over the last several years.

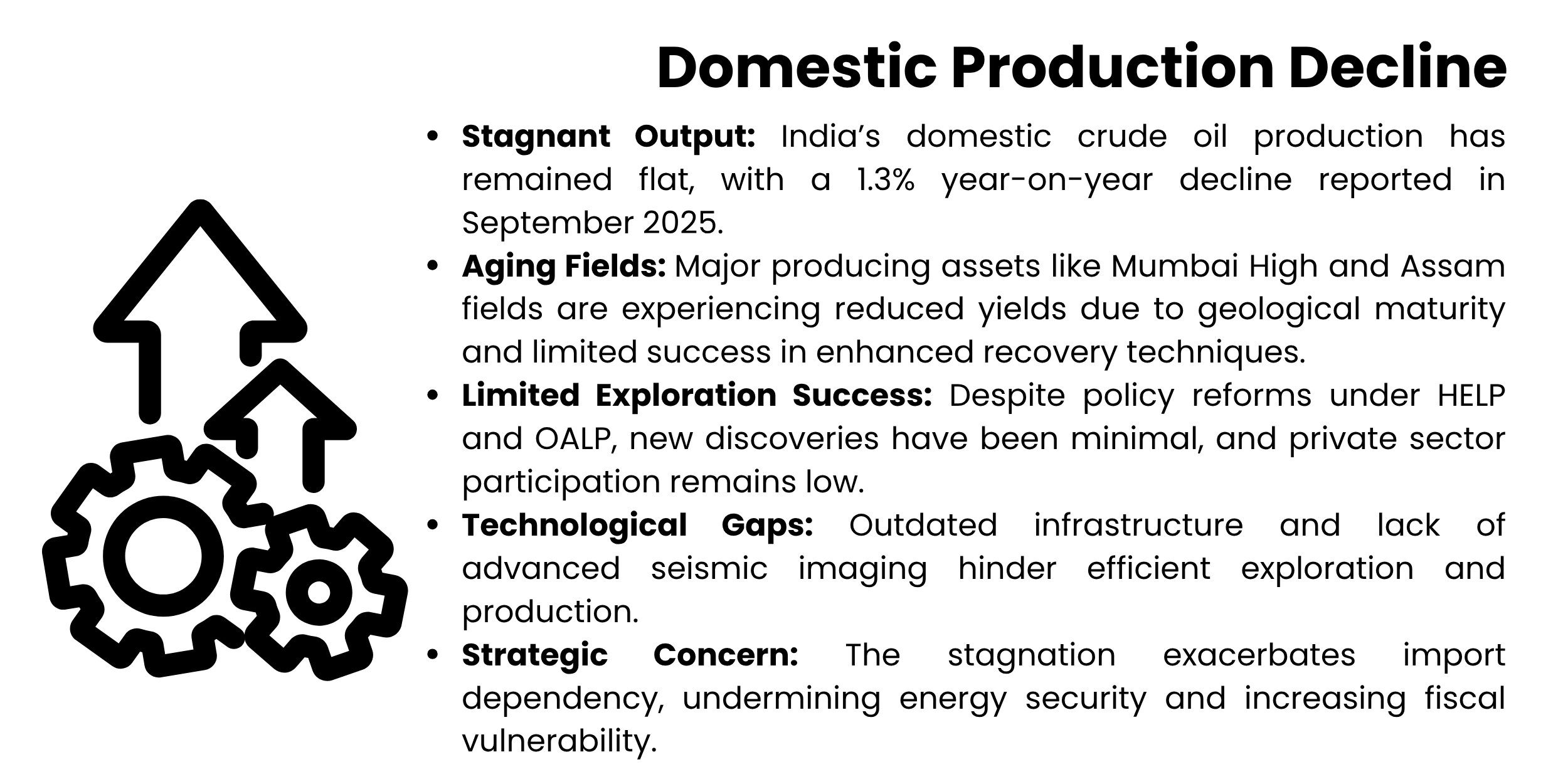

- No growth in Domestic Production: Volume is declining in areas like Mumbai High, and the domestic production dropped by 1.3 percent year-on-year as compared to the year September 2025.

- Demand Drivers: Economy, increase in the industrial sector, and increase in the utilisation of vehicles collectively drive an escalated demand for petroleum products.

- Limited Substitution: Although renewable energy sources and biofuels have not lowered the demand for crude oil, especially in the transportation and industrial sectors, this has not been significant.

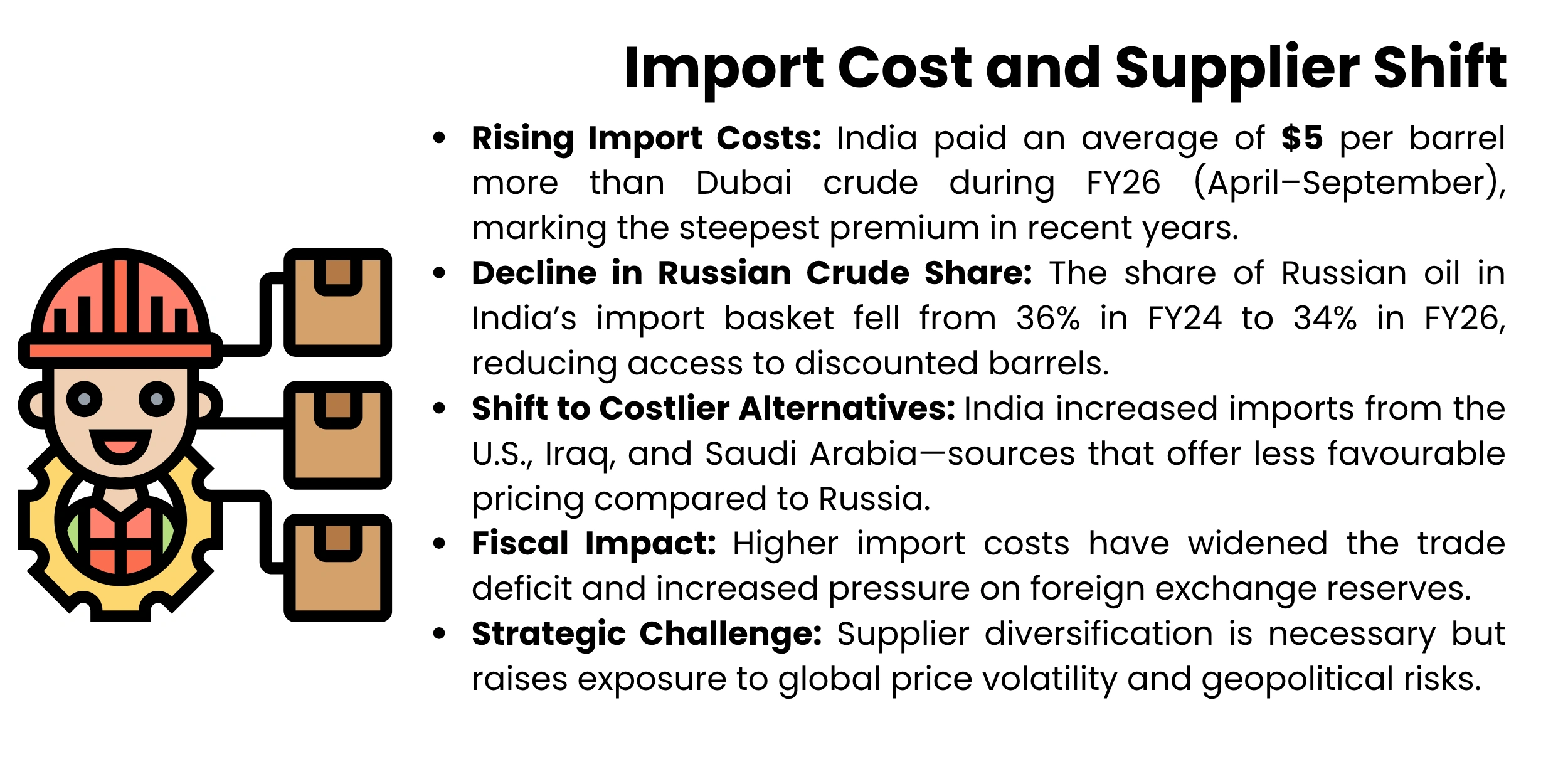

- Geopolitical Risks: Indian dependence on a smaller share of Russian oil and increased reliance on more expensive options puts the country at risk related to disruptions in supply and strategic weaknesses.

- Strategic Responses: Strategic Petroleum Reserves (SPR) expansion, supplier diversification, and exploration and production policy reforms have been initiated.

|

The energy sector in India is undergoing a severe makeover, which is typified by a steady increase in dependence on crude oil imports. Despite organized efforts to diversify the energy sources and increase the domestic output, the reliance of the country on imported crude oil is only getting deeper. This is driven by aggressive economic growth and increasing demand in the transport, industrial, and electrical sectors. The beginning of the current FY (April-September) has already seen a slight trend in the growth of the volumes of imports, and the analysts project that the yearly dependence may slightly exceed the present rates that were already seen during the previous fiscal year. The phenomenon marks an imbalance in production on the local consumption front. The country is mostly stagnant in terms of domestic production because of the fact that the existing oil fields are on the decline, private actors have limited contributions to make, and there is an internal stagnation concerning the exploration and production policy. The growing gap between demand and the native supply has had significant geopolitical, financial, and energy security implications for India. The energy policy, which has been based on importation, puts India at the exposed side of extensive global oil markets with consistent volatility and price spikes.

Therefore, this Article will provide a critical analysis of the factors supporting the rise of imports of crude oil, the decline of national production, and the policy needs to reduce systemic weaknesses. It aims at providing a detailed explanation of the dynamic and policy pressure that defines the dependency of crude oil in India in FY26.

Present-Day Tendencies of Import Dependency

The trend of increasing imports of crude oil in India has been defining the upward trajectory, and it shows a structural imbalance between the production within the country and the rising consumption.

An Increase in the Import Reliance

In FY26 (April-September), India relied on crude oil imports at 88.4% compared to 87.9% in the corresponding period of FY 25. This trend continues a long-term trend, as the dependency levels increase to 87.8 percent in FY24 compared to 83.8 percent in FY19. Analysts in the industry expect the number in the years to come to be slightly higher than the one in April-September of FY 26, in line with the pattern during the previous fiscal years. This growth is explained by the fact that domestic demand has been growing steadily, and production among the indigenous population has not kept up with consumption.

Demand-Led Import Growth

A high dependence on imports is strongly linked with the increasing energy needs of India. Recoveries of the economy, growth and development of industries, as well as mobility, have fuelled in consumption of petroleum products. Although efforts are being made to make alternative fuel and electric mobility, crude oil continues to be the hallmark of the Indian energy mix. India imported more than 101 million tonnes of crude oil in the first half of FY26, highlighting the size of the demand. This pressure on demand has surpassed the domestic supply potential, which underpins dependence on foreign sources.

Cost and Source Dynamics

The cost of imports has also increased; the average price of crude imports in FY26 till today is already 5 USD per barrel higher than Dubai crude, the highest premium in years. Part of this growth can be blamed on a fall in discounted Russian oil, and an increased dependence on even costlier substitutes like U.S. and Middle Eastern crude. The change in the supplier mix has also increased fiscal stress, although the world market oil prices have been fluctuating.

Prognosis and Future Visions

Considering the trend in demand and the lack of growth in domestic output, demand for imports in India should continue to be high during FY26. This tendency suggests the energy security issue, trade deficit, and geopolitical susceptibility. The only way to reduce long-term risks is to diversify suppliers strategically and expedite the exploration of the country.

Drivers of Increased Demand

The growing dependence on imported crude oil by India in FY26 is reflected by a complex interplay of the demand-side factors.

Economy and Industry

The strong macroeconomic performance of India in FY26 has played a significant role in increasing the level of energy consumption. In the first quarter of FY26, the country registered a 7.8 percent year-on-year increase in gross domestic product, the fastest growth since the fifth quarter. This expansion has been intensified by high levels of manifestation in the manufacturing, services, and infrastructure sectors, which are all energy-intensive. Industrial production is also increasing, thus the requirement for the quantity of diesel and ancillary petroleum derivatives, driving the need to have more crude oil imports.

Trends in Transportation and Mobility

The transport sector is one of the major consumers of petroleum products, which are mostly diesel and petrol. The diesel demand in September 2025 alone had grown by 6.6 percent on a year-on-year basis, and the consumption of petrol had also risen by 8 percent on a year-on-year basis. These figures represent an increased level of vehicle movement, both commercial and personal, in the economic recovery and logistics needs pertaining to festive seasons. Despite the policy efforts to facilitate the growth of electric vehicles, internal combustion engines remain the dominant factor in the mobility market of India, and they keep supporting the high demand for refined crude products.

Little Replacement by Substitute

Though India has had striking progress on the deployment of renewable energy, the substitution effect on the demand for crude oil is limited. The electricity generation mainly relies on solar and wind power, but crude oil is necessary to satisfy transport fuel, petrochemical, and heating needs in industries. The slow adoption of biofuels and compressed natural gas (CNG) in the rural and freight sectors also makes the shift to fuel not based on petroleum difficult. As a result, there is a structural dependence on petroleum products.

Refinery Utilization and Strategic Stockpiling

The strategic petroleum reserves (SPR) and the utilization rates of refineries in India have also determined the imports. Due to volatility in global oil prices as well as looming geopolitical risks, India has upgraded stockpiling to act as a buffer to the disruption of supply. Additionally, the high refinery throughput that is driven by the domestic demand and export-oriented refining has resulted in the need to take crude imports to maintain the operating efficiency.

The Stagnation in Internal Production

The fact that India is currently increasing its dependence on importing crude oil in FY26 is not just a result of the increased demand in the country, but can also be explained by the lack of rapid growth in local production.

Lack of Private Sector involvement

This is despite policy changes that have been aimed at liberalising the upstream industry, where the inflow of investments by the private and foreign investors in exploration and production (E&P) is still very low. The growth in the number of explorations has not emerged as envisaged by the policy documents: the Open Acreage Licensing Policy (OALP) and the Hydrocarbon Exploration and Licensing Policy (HELP). High regulatory burden, lengthy gestation, and unpredictable payoff have deterred the entry to the game by the private players, and the state-owned companies like ONGC and Oil India Limited have to bear most of the production tasks.

|

The Government of India has issued the Hydrocarbon Exploration and Licensing Policy (HELP), which was promulgated in an attempt to make a radical change in the regulatory framework. The HELP was supposed to take the place of the old New Exploration licensing Policy (NELP), in order to make things simpler in the exploratory and production (E&P) industry through implementing a regime that is much easier to deal with as an investor, and also in terms of the transparency of the industry.

HELP is based on four main pillars; a standardized licensing approach to all types of hydrocarbons such as oil, gas, coal bed methane, and shale; the open acreage policy to allow companies to choose exploration blocks without using formal bidding rounds, the revenue sharing contract to avoid the profit sharing system and the liberation of crude oil and natural gas marketing and pricing. These reforms were planned to be in such a way that they would be appealing to domestic and foreign investment, reduce bureaucratic barriers, and strengthen domestic production.

Despite the supposedly liberal structure, HELP has had to face problems with implementation, in particular, the low adoption of exploration blocks and long project rating processes. It is, however, still part of the Indian strategic plan to reduce reliance on imports and increase the local hydrocarbon production, especially in the deep-water and frontier basins.

|

Infrastructure and Technology Limitation

In India, the upstream oil industry is faced with the usual infrastructural threats and a technology alternative shortage. Large quantities of onshore and offshore wells have not been equipped with state-of-the-art drilling and reservoir management, and thus recovery rates are suboptimal. Moreover, there is the issue of logistics in isolated areas such as the Northeast and offshore reaches of the Bay of Bengal that reduce the efficiency of operations. Lack of advanced seismic imaging and data analytics further shortens the success of exploration.

Policy Inertia and Implications for Strategy

Despite the incentives that the government has said would be used to spur E&P activities, there have been delays in implementation, and bureaucracy has stalled the process. The current local production has some strategic consequences: it puts fiscal pressure due to an increase in imports and weakens the energy security in the country. Without a firm dedication towards upstream investment as well as technological modernization, it is expected that India will become further reliant on imported crude.

Implication and Strategic Responses

- Fiscal Implications: The increased dependence on imported crude oil has direct implications for the fiscal well-being of India. As the world oil prices continue in a volatile state and the average cost of imports in FY26 is 5 dollars per barrel above Dubai oil, this has increased the import bill. The trend worsens the current account deficit and intensifies pressure on inflation, especially in the transport and manufacturing industries.

- Geopolitical Vulnerability: The energy policy in India is facing the threats of geopolitics more often. The fall in the presence of discounted Russian crude, from 36% in FY24 to 34% in FY26, has forced it to switch to more expensive sources like the United States and the Middle East producers. Despite the fact that this diversification is put in place ostensibly, it increases awareness of the shocks of supply chains, conflicts in the region, and manipulation of prices by oil-exporting nations. The inability to sign any long-term bilateral energy deals further limits the bargaining strength of India in the world markets.

- Diversification and Strategic Petroleum Reservoirs: To absorb external shocks, India has increased its Strategic Petroleum Reserves (SPR) as well as diversified its crude basket. In concurrence, the government stimulates demand substitutes like the additions of ethanol blending, compressed biogas (CBG), and the benefits of electric mobility infrastructure through government programs like SATAT and FAME. These measures have a vision of reducing reliance on crude oil in strengthening energy resilience. However, their effect is still in the increase stage and is not enough to offset the pressure on imports in the short term.

- Upstream Investment and Policy Reform: The stagnation in domestic production has been recognized, and the government has proceeded to reform the policies aimed at preserving investment in the exploration and production activities. Some of the measures include liberalized licensing as a part of the HELP system, enhanced data access, and financial incentives to deep-water and frontier basins. These projects play a crucial role in reviving local production and reducing the reduction in the export-led character of imports in the long run.

Conclusion

The fact that India has increasingly been engaging in the reliance of imported crude oil in FY26 evidences a structural imbalance between the level of production in India and the rising energy demand. The country is still vulnerable to the external effects of prices, fiscal strains, and geopolitical risks despite deliberate initiatives and diversification endeavours to cushion the country against such dynamics. To reduce the risks in the long term, it is crucial to enhance domestic exploration, increase strategic petroleum reserves, and speed up the process of energy transition. A multi-pronged strategy is crucial as it is calibrated to ensure energy security, maintain economic resilience, as well as sustainability within the ever-changing oil environment in the world.