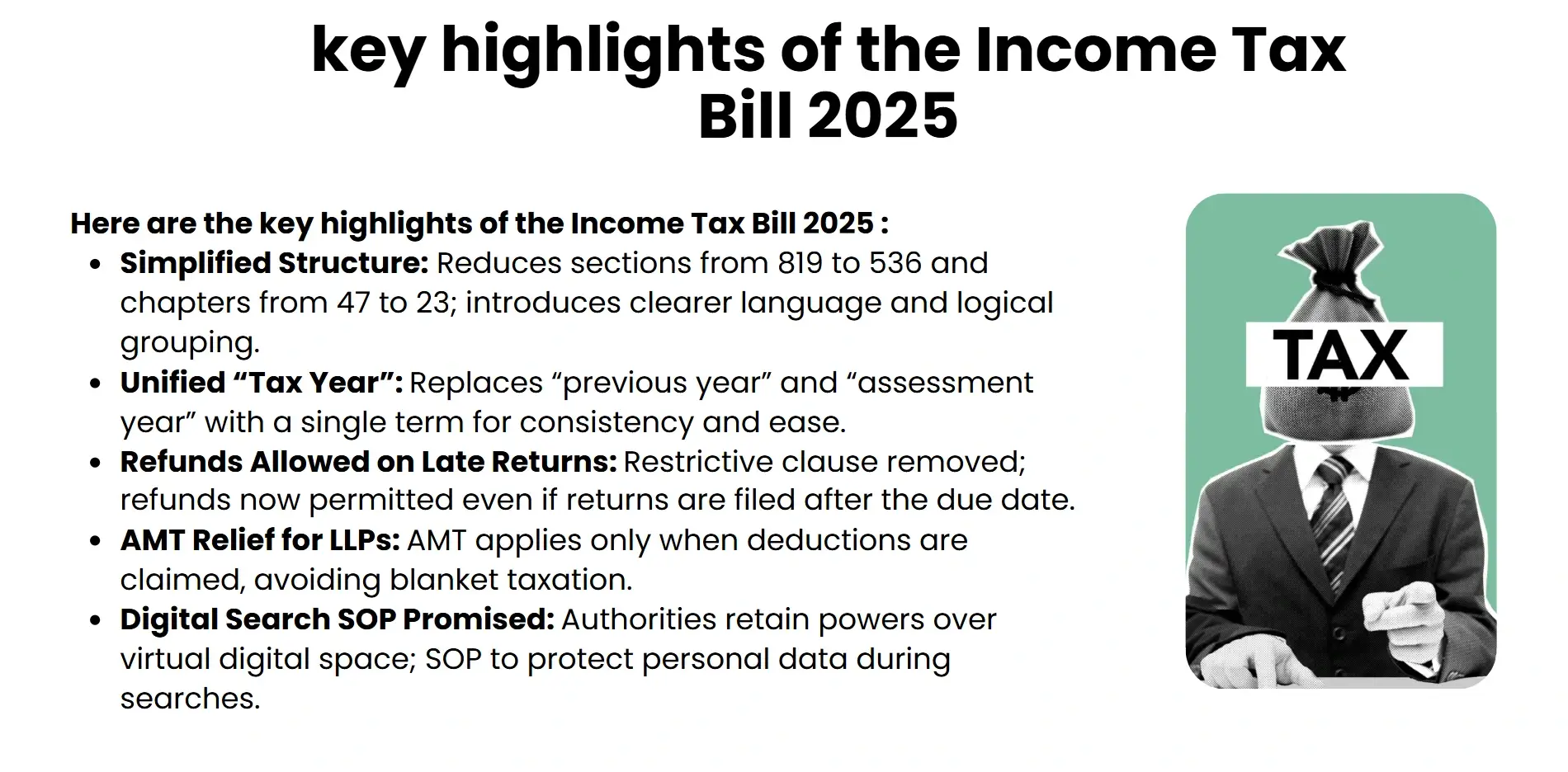

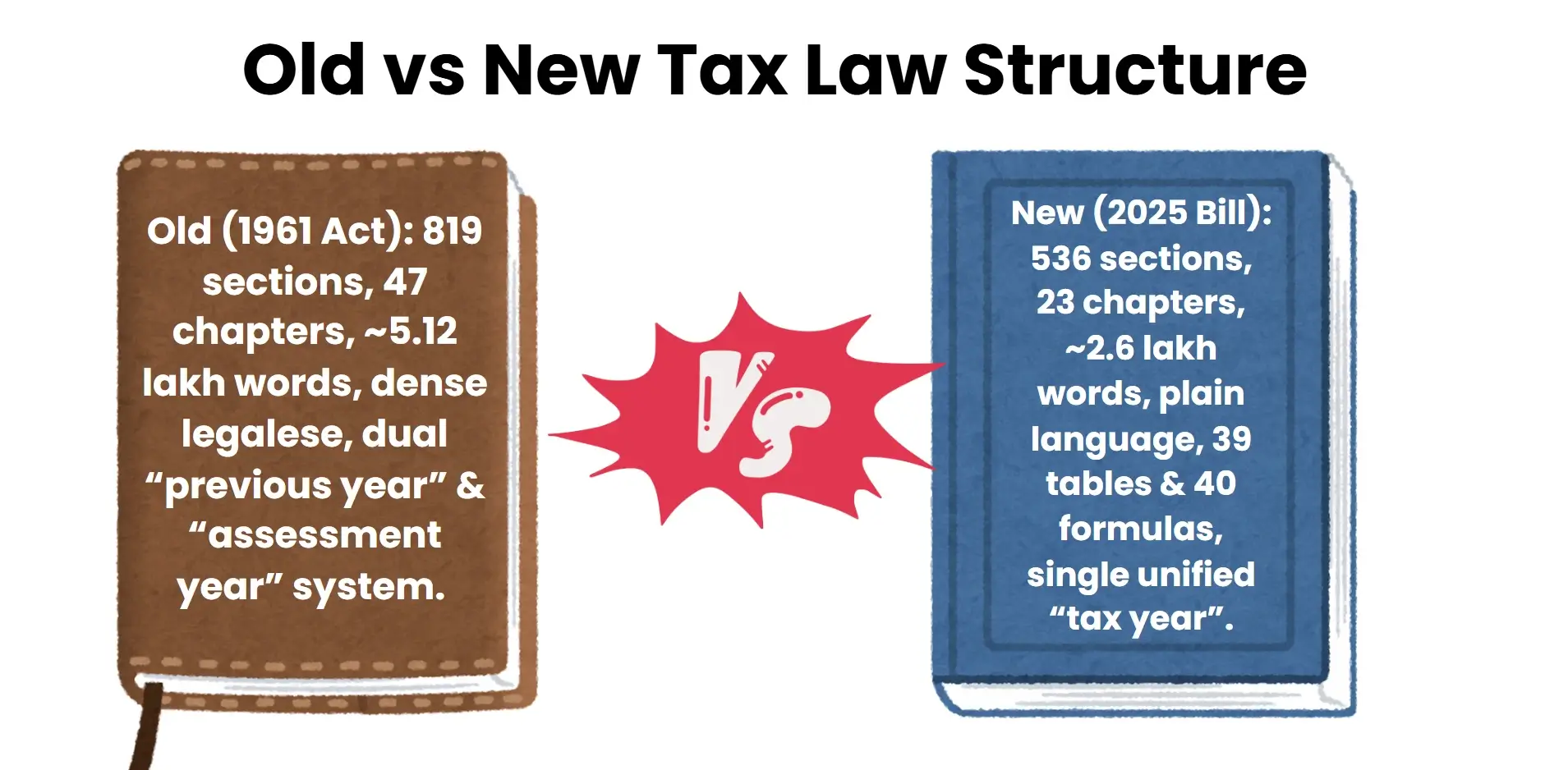

The Income Tax Bill 2025 became law after the parliament simplified the 1961 law and better explained how to get a refund, what deductions and compliance rules there were to follow-effective April 1, 2026.The new bill aims to simplify not only through language but also by reducing the bulk.For instance, the old Income Tax Act had 819 sections, but the new Income Tax Act has only 536 sections3. Moreover, the number of chapters is also brought down from 47 to 23.

Nearly seven decades later, the Indian income tax law is being restructured to a massive extent. On Tuesday, the Income Tax Bill, 2025, ushered in a slimmer, more transparent and simplified structure, replacing the Income Tax Act of 1961, by passing through Parliament. The new tax program, which will run beginning April 1, 2026, slashes sections and chapters by almost fifty percent, adds the concept of a single “tax year,” and tries to make compliance simpler for individuals, businesses, and institutions that are charitable. The Bill also introduces substantial procedural changes, even though the tax rates will remain the same,including refunds on late filers, reinstated NIL TDS certificates, and reduced correction time periods on tax statements.In case of salaried individuals and home owners, deductions of house property and pensions have been clarified in the Bill and companies will get the benefit of the rectified provisions of inter-corporate dividends and alternate minimum tax (AMT) of LLPs. Charitable trusts enjoy more transparent regulations on how their income is applied, or even anonymous giving. Notably, the Bill gives wide search over digital powers but has committed a standard operating procedure (SOP) to protect the personal information.This article lists major provisions of the new law, what is changing as well as what is not changing to the taxpayers. With the Indian implementation scheduled in 2026, these reforms would be useful in financial planning, compliance, and informed discussion in the circle of the population.

The structural rewrite

The Income Tax is a major shift in the way the Indian tax law is conceived and understood. In addition to rates and refunds, simplification of the law itself is the most fundamental way in which it has changed.

Complexity to Clarity

Compared to the old Act, the new one has a quarter of the number of sections (819 to 536) and chapters (47 to 23), almost a half in legal volume. This simplification is because it is a conscious attempt to streamline and eradicate duplication or consolidate similar provisions, and stipulate the tax law in a more palatable form. The overall amendment also includes 39 tables and 40 formulasin order to make the calculations less complicated and narrow the scope of the law to people who are taxpayers and lack legal knowledge.The Income Tax Bill, 2025, is a radical change in the organization and interpretation of tax law as followed by India. In addition to rates and refunds, the most radical aspect of it is the simplification of the law itself by architecture.

Unified Tax Year

Among the most interesting and important alterations, the elimination of two terminologies, namely, previous year and assessment year, and their replacement by a sole terminology, tax year, appears as one of the best changes. This is in line with the financial year (April-March) and does away with a long-standing cause of confusion over taxpayers and professionals. Tax year has now become the point of reference when it comes to income calculation as well as taxation, thus making it easier to correct documentation and adherence.

Faceless-First and Digital-Ready Framework

The Bill strengthens the move of India to faceless assessments and e-Tax administration. Although such procedures were initiated previously, the new law integrates them into the framework of the order so that the default settings in the future are digital interfaces, e-verification, and remote scrutiny. This not only minimizes the discretionary power but also increases transparency and the convenience of taxpayers.

Refunds, filing, TDS

The Income Tax Bill 2025 makes a number of taxpayer-friendly modifications that pertain to refund and filing requirements as well as TDS compliance. These reforms are designed to alleviate administrable obstacles and maintain crucial protection.

Belated returns permitted

To the great relief, the new law also gives a chance of a refund even to taxpayers who incur tax after paying their taxes belatedly. This undoes a non-refundability provision in the previous draft that deprived belated filings of a refund. Individuals who are failing to file their returns on time now have an option to get the excess tax (TDS included) back. Nonetheless, the provision (Section 433) requiring that a reference be submitted torequest any refund is kept intact by the law;no other mechanism is envisaged. This implies that every individual, such as the aged, whose income is less than the exemption limit, should continue to file returns just to get back the amount of tax deducted.

NIL TDS Certification Reinstated

The Bill also points to reintroducing the provision of NIL TDS certificates, enabling the taxpayer not have any tax liability to get an advance clearance by the tax department. This is forresident as well as non-resident taxpayers. This will minimize unwarranted deductions and enhance cash flow, particularly among those retired, on a freelance basis, and those earning low income.

No Penalty for Late TDS Statements

The other favourable development is that now there can be no financial penaltiesfor late filing of TDS statements. Delays that were not liable to tax before were once subject to fines. The sanction will be gone with the new law that recognizes that missteps in the process should not cost a penalty. Also, the correction window of TDS statements has been shrunk to two years as compared to six, which motivates prompt corrections to be made.

Compliance Relief with Caveats

These reforms make compliance easier, though they do not go all the way to making low-income people not have to file returns in order to claim their refunds. Relief on such a scale had been proposed by the Select Committee, and it was not taken. Therefore, it has become easier to understand the procedures, although no changes in the filing requirements have been implemented.

Individuals, homeowners, businesses, LLPs, and professionals

In the Income Tax Bill 2025, there are specific improvements made to individuals, property owners, and business entities based on transparency, uniformity, and avoidance of procedure.

Individuals and homeowners

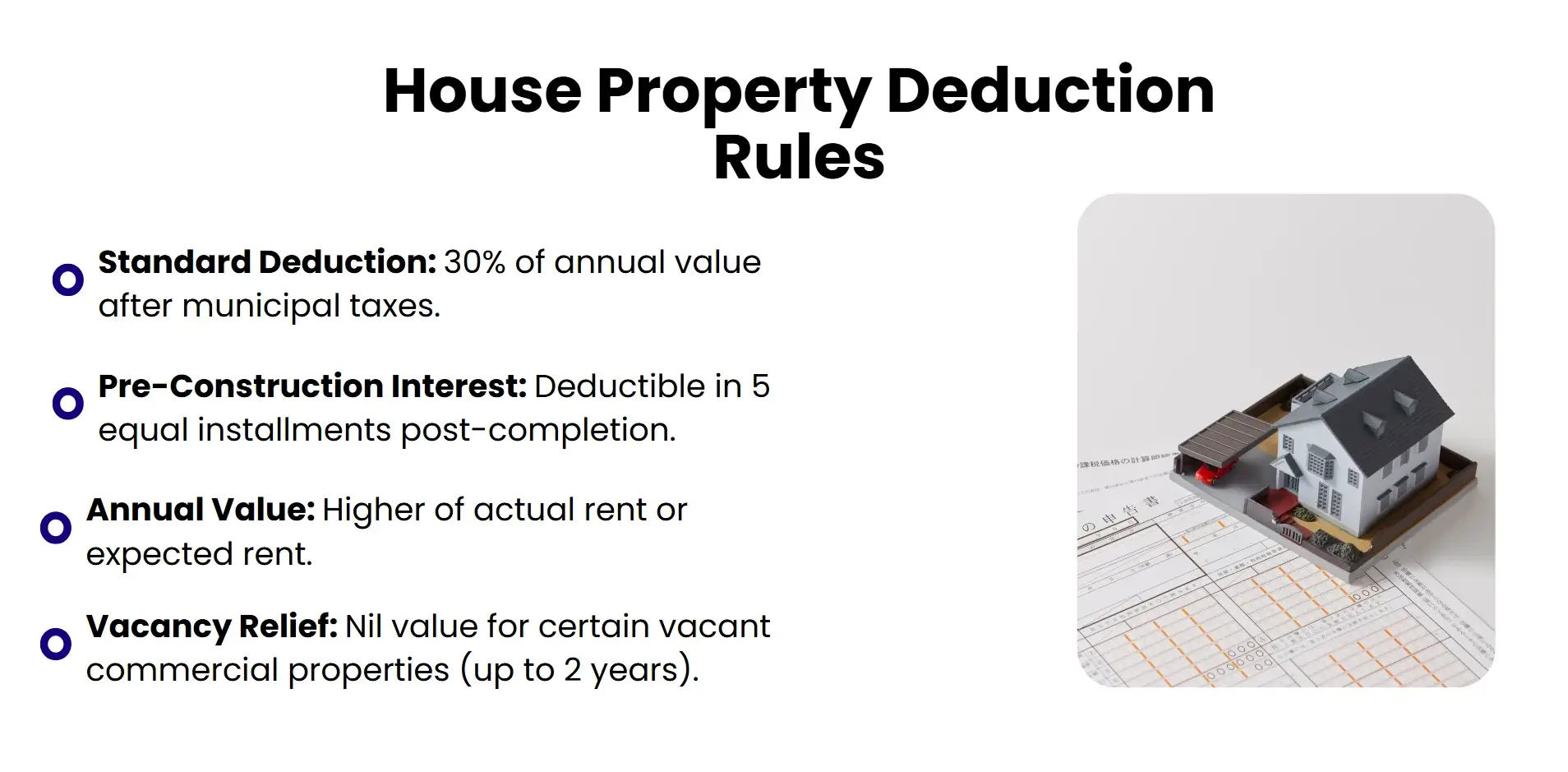

To those salaried people and house owners, the Bill refutes ancient ambiguities of properties. It claims that Clause 22's confirmed 30 percent standard deduction on annual value after municipal taxes. Interest on purchase, construction, or repair loans isdeductible, and pre-construction interest is unamortized over five years. In a self-occupied house, the interest limit is ₹2 lakhs (under conditions) or ₹30,000 in other cases.

The actual rent range on the property today is considered to be the higher between the actual and expected rent value to diminish the conflicting views on its notional income. There can be deferral of treatment as having nil annual value up to two years after completion of commercial properties awaiting business tenants in situations of a delay in the tenant taking, or after conversion, the tenant delaying refurbishing the completed property: in each case, the properties concerned may be held as stock-in-trade.The other pension reforms entail the complete exemption of the commuted pensions, which were applicable to both the government and the privately employed workforce.

Businesses, LLPs & Professionals

Corporations benefit from the Bill, which restores Section 80M to be able to deduct inter-corporate dividends even in the concessional tax regime, which eliminates cascading tax. Another drafting mistake in the previous version has now been remedied: LLPs deriving all their income as capital gains are no longer subject to Alternative Minimum Tax (AMT), except when they make deductions.

The new rule requires professionals with receipts exceeding 50 crores to start using prescribed electronic methods of payment, and,similar to large businesses, this makes payments more traceable digitally. The Bill also splits off MAT and AMT provisions to make them clearer and brings updates to the rules on transfer pricing to make them less subjective.

Non-Profit organizations (NPOs) and Trusts

The Income Tax Bill 2025 provides a unified and more transparent taxationstructure on charitable trusts and non-profit bodies in order tominimize confusion, ensure efficient compliance, and make tax exemptions more taxpayer-friendly based on the interest of the community.

Consolidated Framework to Registered NPOs

The Bill recreates these disparate pieces of the 1961 Act and so provides a single chapter (Part B of Chapter XVII) devoted to registered non profit organizations. Such consolidation puts rules on registration, income application, donations, and compliance under one umbrella, and this makes it easy to navigate through the tax liabilities of trusts, societies, and the Section 8 companies. The name of a registered non-profit organization is now used consistently to mean entities that are registered under sections 12A, 12AB, and 10(23C), thus eradicating confusion between classes.

Anonymous Donations

One of the important changes is anonymity of donations. The Bill has reintroduced the exclusion of donation, which is provided to purely religious trusts that was given by the Select Committee. Nonetheless, the mixed-object type of trusts; that is those which carry out the running of hospitals, schools, or other charitable activities in addition to performing religious activities will have such donations taxed at a flat rate of 30%. This is meant to discourage abuse without having to destroy the contributions associated with the religions.

Use of Income and Real Income principle

Provision of the Bill as to what is income is clear that the reinvestment of capital gains and expenditure on charities are included under the application of income. It also eliminates the previously made proposal of taxing gross receipts thus reinstating the principle of real income; only net income is subject to tax. This will guard NPOs against disparate taxation and is consistent with the well-established jurisprudence.

Simplified compliance

Although the Bill does away with complicated registration and audit processes, NPOs need to be wary of slip-ups in procedures. Inability to file returns or reinvest acquired money by transferring parts of the assets might lead to total taxation of income.

Other notable Provisions

Among the other less talked about, yet effective, modifications is the passing of Section 80M, which allows corporations to take a deduction on inter-corporate dividends even in the concessionary 22 percent rate scheme. This prevents tax pyramiding in complex corporate entities. Another element of the Bill is to make advance tax interest provisions concur tothe current law which took a step toward overcharging interest in order to cover slight disregards.

With a cap of 60% of the corpus being tax-free at retirement, UPS and NPS share the same status with regard to pensioners. Additionally, the Bill provides for commuted pensions to be fully tax exempt for approved funds, not just for salaried employees.

In order to reduce the likelihood of litigation, the Bill also adds the MSME Act's definition of MSMEs, does away with the current automatic system that requires a 15 percent deposit to legitimately cover itself as deemed accumulation by the trust, and shortens the time frame for TDS correction to two years.

What Hasn’t Changed & What to Watch

Tax levels and slabs are not changed even after the structural adjustments. The new regime carries forward the 12 lakh notax limit and standard deductions as under Budget 2025. The Bill leaves unaffected capital gains provisions, rate of surcharges and exemption of foreign investors Section 23FE.

Following the implementation is what to watch. The Central Board of Direct Taxes (CBDT) has to formulate elaborate rules, revise forms, and give out a Standard Operating Procedure (SOP) to deal with digital data seized when the searches are made. Transfer pricing definition changes should also be watched by the taxpayers and more particularly, the definition on what is an associated enterprise, which could also broaden the scope of compliance.

Conclusion

The Income Tax Bill 2025 is a milestone change to the Indian fiscal framework- replacing a sixty-year-old legislative framework with a lean, digitally integrated and taxpayer-friendly model. Although it does not involve changes in tax rates, its focus on clarity, less litigation and procedural relief is a major milestone towards the modernization of tax governance. Individuals will see their deductions clarified and their refund eligibility aptly determined, companies will receive structural adjustments such as AMT relief and exemptions on dividends, among others, and trusts will experience consolidated rules on compliance. The test, though, will come later: whether simplification translates into ease through effective implementation,timely rule-making and education of the taxpayers. Since the law is supposed to start to operate on April 1, 2026, it will require stakeholders to transition the new law by familiarizing themselves with new definitions, digital processes, and compliance deadlines. India is progressing towards a more transparent and open access tax policy, and the Bill is a promising step in the right direction, although it will succeed or fail on its implementation, flexibility and dialogue between policymakers and taxpayers.