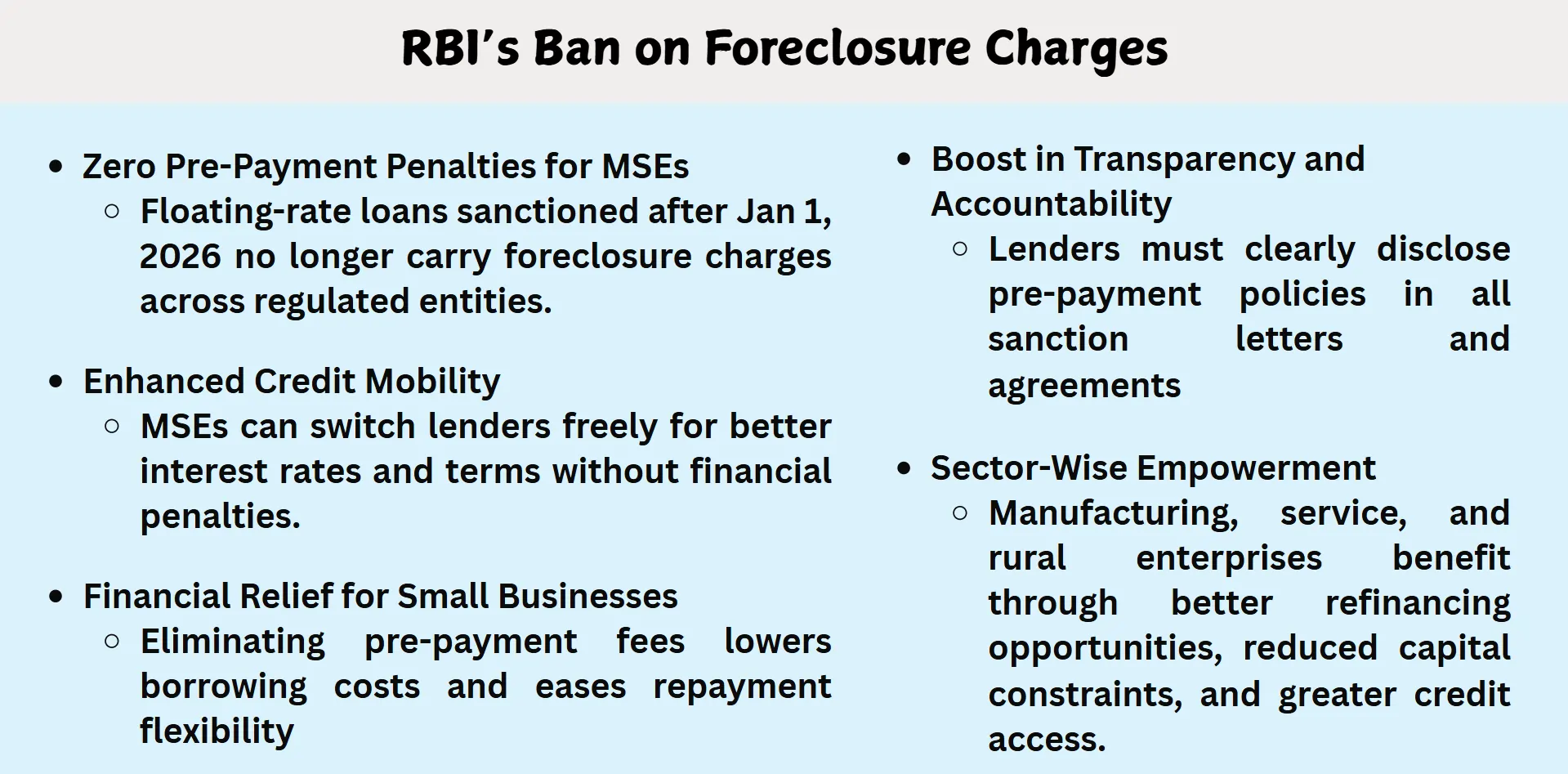

The directive issued by the RBI prohibits the imposition of foreclosure charges on floating-rate MSE loans which is part of its effort to enhance credit portability, transparency and affordability of small business.

This is a major decision that will certainly help empower the banking system of India to support the micro and small enterprises (MSEs) since the Reserve Bank of India (RBI) has issued new guidelines that ensure that floating rate loans to the MSEs do not incentivize foreclosure charges. Anyone to change this regulation, as it is proposed that it is to become law on January 1, 2026, regulated institutions such as commercial banks, upper-layer NBFCs, and Tier 4 urban cooperative banks should cease to charge pre-payment penalties in the event that MSEs wish to repay their loan before the agreed date. Such choice comes out of the RBI supervisory surveys that indicated extensive fragments and restrictive activities in lending institutions which frequently left the borrowers favouring and challenging.Since there are more than 6 crore MSEs that play a significant role in employment generation and contribute to the growth of the GDP, the directive will alleviate financial burden, in addition to credit mobility and transparency in loan acceptances. By eliminating penalties to early repayment, it enables business people to access more competitive quotations, which may transform the lending environment. In principle, the reform is not only a testament to RBI maintaining its stance of making its banking inclusive, responsible, but also establishes a precedential example as to how systemic barriers to MSME credit in the Indian banking system can be overcome. This Article discusses the reasoning, consequences, and prospects of the prohibition of foreclosure fees - and its general effect on the stability and prosperity of small businesses.

Understanding RBI’s Directives

The recent directive issued by the Reserve Bank of India in July 2025 seeks to prevent floating-rate loan foreclosures to the Micro Small Enterprises (MSEs) a long-standing problem of credit flexibility and disclosure.

- New Guidelines: Within this regulatory environment, any floating-rate loan sanctioned or renewed to MSEs from January 1, 2026, is exempted of any pre-payment penalty. This action is extended to the commercial banks, non-deposit taking NBFCs under the upper (NBFC-UL) category, and Tier 4 city urban cooperative banks. It is worth noting that the provisions are geared towards making lending practices uniform and, reduce predatory clauses which did not allow borrowers to change lenders easily.

- Exemptions and certain Inclusion: As much as the directive is extensive, there still are some of the categories which are partly exempted. These are;Small Finance Banks, Regional Rural Banks and the Middle Layer NBFCs where the ban on pre-payment charge is only applicable on loans of a maximum of amount of 50 lakh. This shows the staged approach of the RBI that reflects an equal consideration of the enforcement of the regulator and the sector.

The Supervisory Findings and Intent of RBI

- Determination of Divergent Practices: The directive is premised by the fact that observations by supervisors indicated that advance payment policies in regulated entities which were not uniform. Most of the institutions included restrictive terms in loan agreements, and this came as a roadblock to MSEs that wanted to be refinanced or to get competitive rates. Such discrepancies often cause customer complaints and lawsuits, emphasizing a change in the system.

- Encouraging the Affordable Credit:RBI wants to give more competitive and the broad-based credit environment by doing away with the pre-payment penalties. The directive will be a supplement of its overarching mission of promoting responsible lending, decrease of costs of borrowing and enable MSEs to make strategic financial moves without compromising fears of punishment.

Motives behind the Move

Move by Reserve Bank of India illuminating the foreclosure charges on floating rate loans to MSEs, indicates a tactical reaction towards regulatory disparities and inefficiencies in the market as well as complaints by the borrowers.

Supervisory Insights

- Different Policies in Institutions: Through internal reviews conducted by RBI, it was found that the various banks and financial institutions have non-homogeneous policies on pre-payment charges. Whereas penalties were heavy imposed by certain institutions, other acted silently by including restrictive kinds of clauses in the loan which restricted the MSEs to be able to refinance and change the lenders. These discrepancies which could at times be hidden in elaborate loan documents, led to a sense of confusion and discontent amongst those taking the loans, especially small business enterprisesthat hardly have access to any financial advice consultations.

- Increase in Customer Complaint and conflict:Its secrecy led to suspicion and legal turmoil in the course of time. Complains about unfair pre-payment terms were also a habitual occurrence that put a strain on the regulatory ecosystem of oversight. The intercession of RBI is therefore an urge in an endeavour to normalize the experience of borrowers and reclaim lender responsibility in the retail credit activities.

Strategic Objectives: Enabling the MSE Borrowers

- Competitive Credit Markets Creation: eliminating penalty foreclosures; portability of credit will be strengthened as lenders will be unable to threaten and new attempt to seek more advantageous rates or terms will be achieved. This creates a healthy competition among lenders and motivates the institutions to concentrate more on retention of their customers in terms of quality service delivery than contract adhesions.

- Bettering the Financial Inclusion and Responsiveness: This directive is also in line with the overall mandate of RBI of ensuring affordable inclusive finance. Small business ventures have low margins. This will minimize inappropriate expenses incurred in credit reshuffling which will enable them to adapt to various dynamics in the market without any penalty charges.

Implications for MSE Borrowers

This decision by the RBI to abolish foreclosure rates on the float-rate loans will transform the process of borrowing in favour of Micro and Small Enterprises (MSEs),opening upbeneficialeconomic and strategic gains.

Financial Liberation and the Economy

- Reduced Burden to Capital-Scarce Businesses: The MSEs are normally having thin margins and limited access to capital. With the removal of pre-payment fees, the borrower is allowed to make payment earlier without any penalty hence it maintains its liquidity and the interest is sold. This relieves the long termfinancial burden and allows small firms to invest the capital on other operations or growth.

- Debt Flexibility: The right to pre-pay or to have a refinance improves management of cash flow. The seasonal needs or changes in the market allow MSEs to restructure their debts to fit business cycles and select their methods of repayment, which makes it possible to avoid the pressure and inflexibility of the lending partners.

Increase in Credit Mobility and Competitiveness

- Less Difficult Change of Lender: In the absence of foreclosure penalties to raise exit barriers, the MSEs enjoy the costless ability to move to institutions with higher rates, higher quality of services, or to more flexible repayment terms. This change means lenders have no choice but to compete on more than price: on relationship management and digital service delivery.

- Bargaining Power Empowerment:Those people who have a clear record of repayment and financial control canbargain for more advantageous terms of the loans. The less rigidity in the contract is interpreted to mean more agency and autonomy of the financial decision-making, which is essential in maintaining the momentum of entrepreneurship.

Clear and Open Lending

Since regulated entities should be compliant with the new directive, pre-payment policies should be mentioned clearly in sanction letters and agreements. This enhances informed borrowing, eliminates legal confusion and enhances trust between lenders and small businesses.

Sectoral Impact Analysis

The policy reform in foreclosure charges done by the RBI will have variouseffect based on manufacturing, service, and rural enterprise whose financial requirement and credit accessing trends are varied.

Manufacturing MSEs: Facilitating Movements of Capital

- Investment-Intensive Operations:Largely, manufacturing business establishments need to have large amounts of upfront capitals on machines, infrastructure and labor. By waiving the fees charged on foreclosures, manufacturers will be able to refinance high-cost loans at better interest rates as well as rationalize the savings into modernization and productivity-enhancement efforts.

- Supporting Scale and Growth: Small manufacturers will be able to engage in a capacity expansion project with more certainty as there are more refinancing opportunities accessible. This causes agility within the industry, whereby these units can expand or even contract in line with the market demand without having the exit penalty scaring them.

Service Sector MSEs: Promoting Fluidity of Finance

- Working Capital Flexibility: The cycles of cash flow of the service- MSEs that come in the form of consultancies in Information Technology and logistical partners are often prone to changes. The directive also gives such companies more freedom to pre-pay when revenues are high or change lenders to turn loans to match short-term business strategies.

- Digital and Start-up Accelerator: Low-friction credit flow is a tremendous advantage to early-stage startups and providers using digital services. These companies will be able to switch financing strategies on the fly with no pre-payment obstacles and thus become increasingly resilient and creative.

Rural Enterprises: Enhancing the Availability of Credit

- Level Playing Field: Historical access through formal credit is limited among MSEs in the rural setting. With the removal of Foreclosure charges the entry and exit barrierswill be reduced and people will have more interest in dealing with the institutional lenders.

- Infrastructure Improves: favourablerefinancing can also motivate rural business to obtain a loan in order to update the infrastructure: this can include storage, transport, or a solar installation which can then enhance the efficiency of operations and long-term sustainability.

Issues and the future

Although the action taken by the RBI to remove foreclosure charges is a landmark policy initiative, its execution will be limited to filling any vacuity in structures, and the upsurge to reach borrower-based modifications, which will have to be upheld.

Implementation Gaps and Exclusion Zones

- Partial Transferability between Institutions: The first short-term challenge is that the scope of enforcement is limited. Those financial entities which are partially covered include Regional Rural Banks and Middle Layer NBFCs, whereas loans facilities that were beyond 50 lakh were not covered. This gives a disjointed picture of lending where MSE borrowers might continue to fall victim to penal clauses based on the type of lender making it all a dampener.

- Uncertainty of the Current Contracts: All loans approved before January 1, 2026 stay under the older conditions. What this implies is that legacy borrowers can still incur foreclosure penalties, except the institutions restructure the aged deals on their own volition to comply with the new directive. These inconsistencies may result in perpetuated grievances and reputational repercussions to the lenders.

The Vigilance, Conformance, and Reform Pace

Possibility of Fee Substitution: Banks could consider other avenues of generating profits (charging more on processing or having hidden charges) to cover the foreclosure penalty deduction. It would be important to ensure simple pricing mechanisms and audit controls that will be crucial in avoiding the exploitative workarounds.

Creating Financial Literacy and Awareness Promotion: The success of policy depends on the understanding of the borrowers. Small businesses have to be informed that they will have rights and negotiate the terms of loans. The use of financial literacy in onboarding and campaigns will help to decrease informational asymmetries and increase the outreach of the directive.

Way Forward: Strengthening Regulatory Wants

RBI may in the future even decide to spread foreclosure charge moratoriums such that it is across all loan categories and lending institutions, resulting in standardized protection of small lenders. This would strengthen inclusivity and ensure that lending is in tandem with the nation's goals of ease of doing business.

Conclusion

This business-oriented guidance by the Reserve Bank of India, to do away with the foreclosure charges on the floating-rate loans of the MSEs, is one of the important moves in the right direction in equalized and borrower-friendly bank credit operations. The RBI makes small businesses a lot more capable of controlling their debts in a smart way and negotiating more reasonable terms of lending since it breaks the financial barriers to loan mobility. In the words of the governor, this step will not only enhance transparency and consistency in the financial institutions but also establish a healthier credit environment where affordability and trust are the fundamental building blocks. But, the real difference will be seen after proper implementation, close monitoring and even further, the unification of the credit norms among all institutions of lending. In the changing and variable currents of India, its MSE sector is facing change, and in this context, these reforms are essential in cultivating resilience, as well as in growing the sector and in making sure that the financial inclusion agenda is not a dream, but a reality in the lives of millions of entrepreneurs.