|

Key Highlights

- Two Slab Simplified tax

- Major Sectoral Cuts

- GST Exemption for essential items

- Compensation cess on Sin and Luxury

- GST Appellate Tribunal

|

The article describes the functions of GST Council, major reforms of its 56th meeting, two-slab GST rates, and Compensation Cess.

|

Relevant Suggestions for UPSC and State PCS Exam

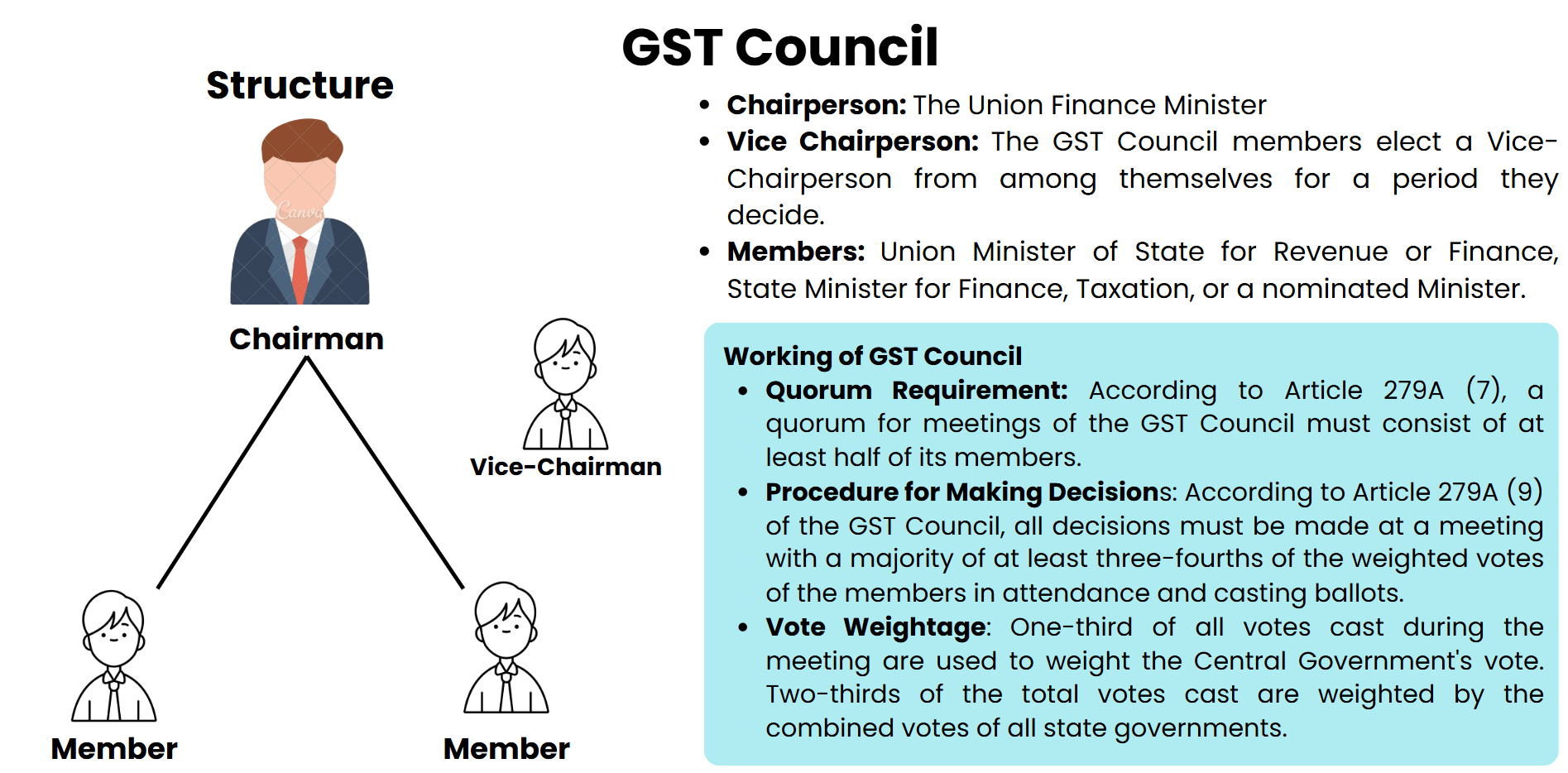

- The GST Council: Constitutional body under Article 279A; the head is the Union Finance Minister, and the representation will be 75% (required to pass Legislation) majority vote by Council.

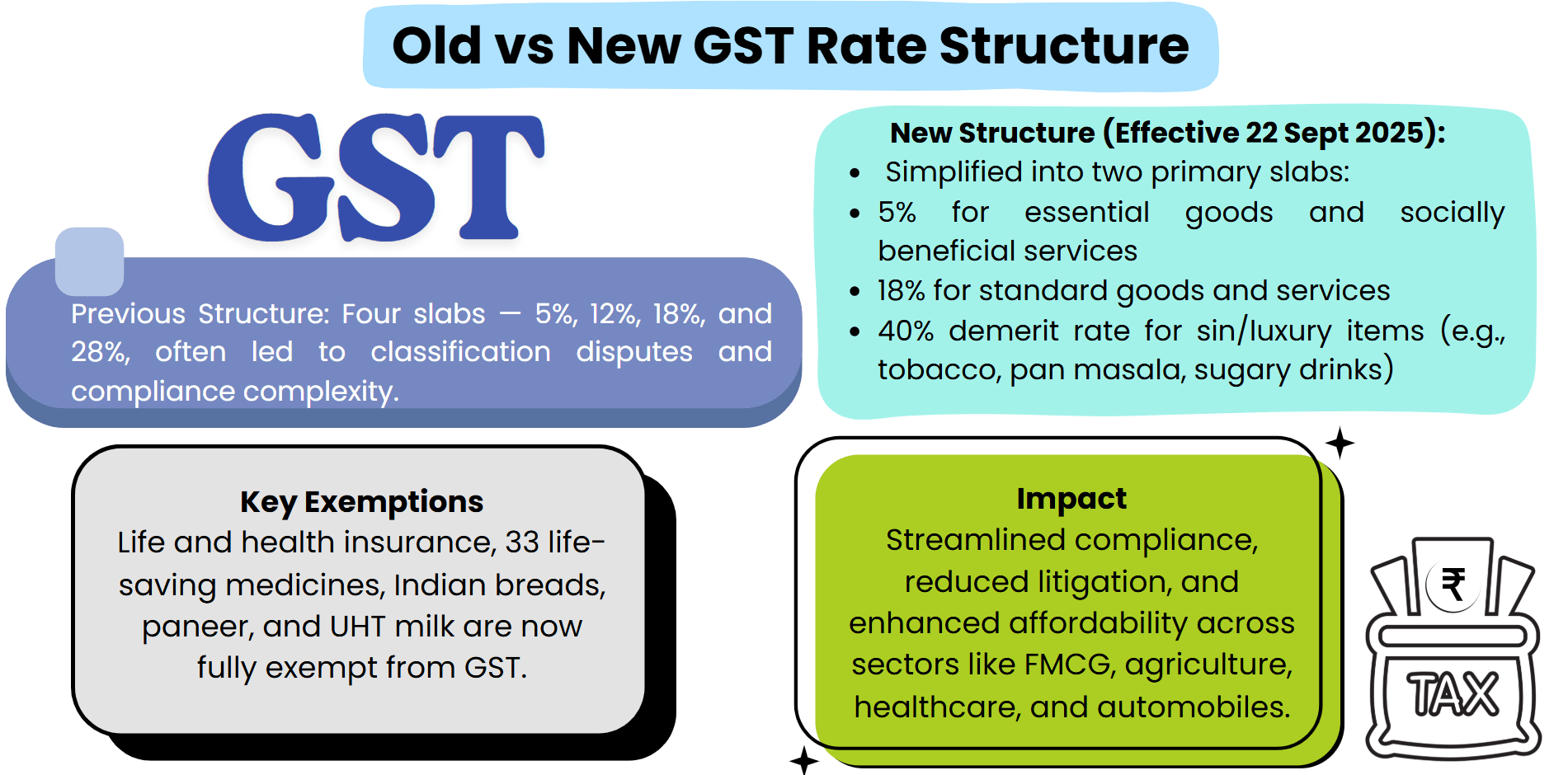

- GST Council Meeting 56: held on 3rd-4th September 2025. Engineered a simplified version of the GST system with the following two-slab GST-structure 5% essentials, 18% normal goods, 40% sin/luxury goods.

Sectoral Reforms

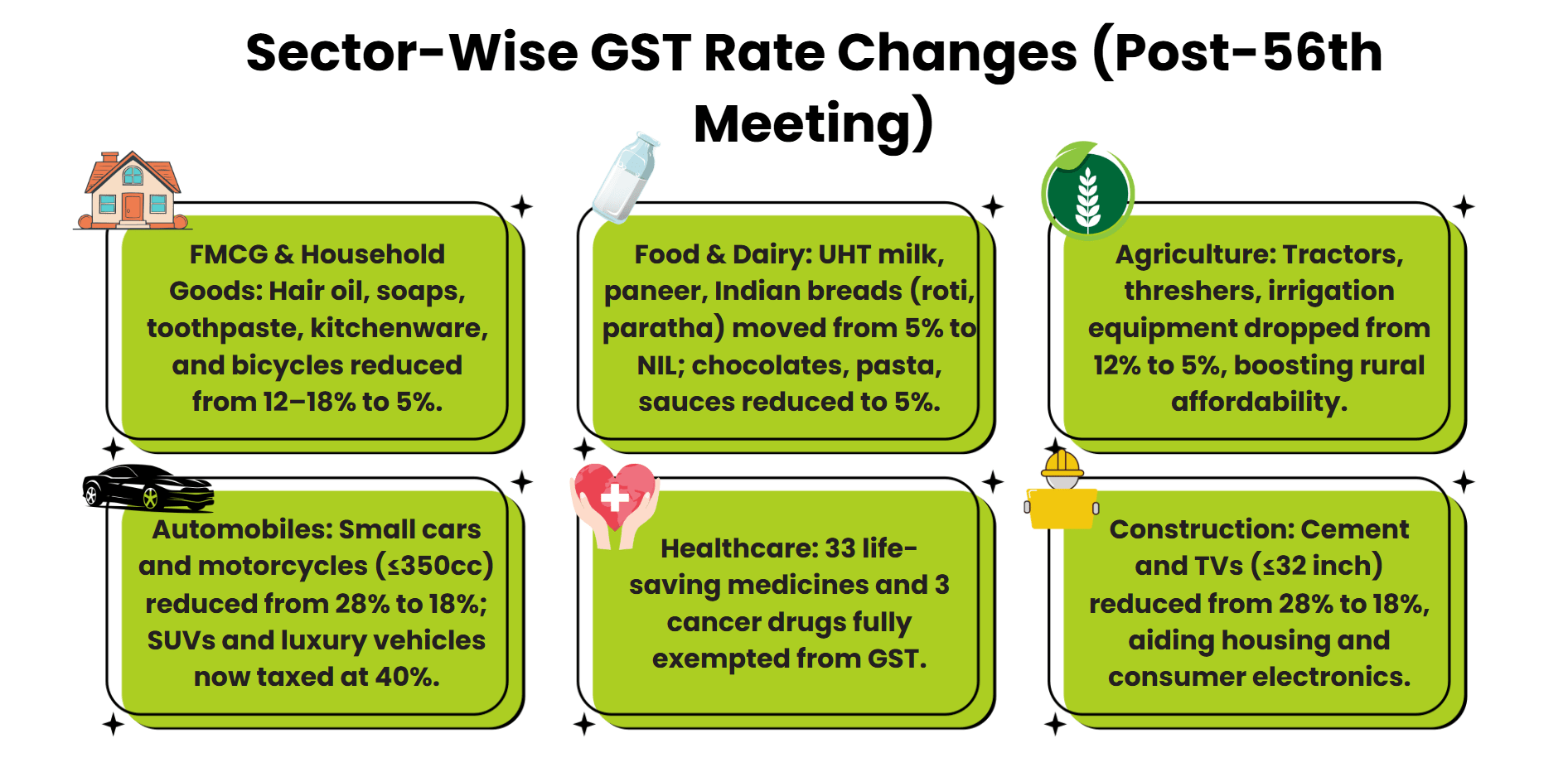

- The rate was reduced in the FMCG, agriculture, and construction fields.

- Dairy products and life-saving medicines were exempted.

- Small cars and two-wheelers may be driven to 18 per cent; luxury vehicles not less than 40 percent tax.

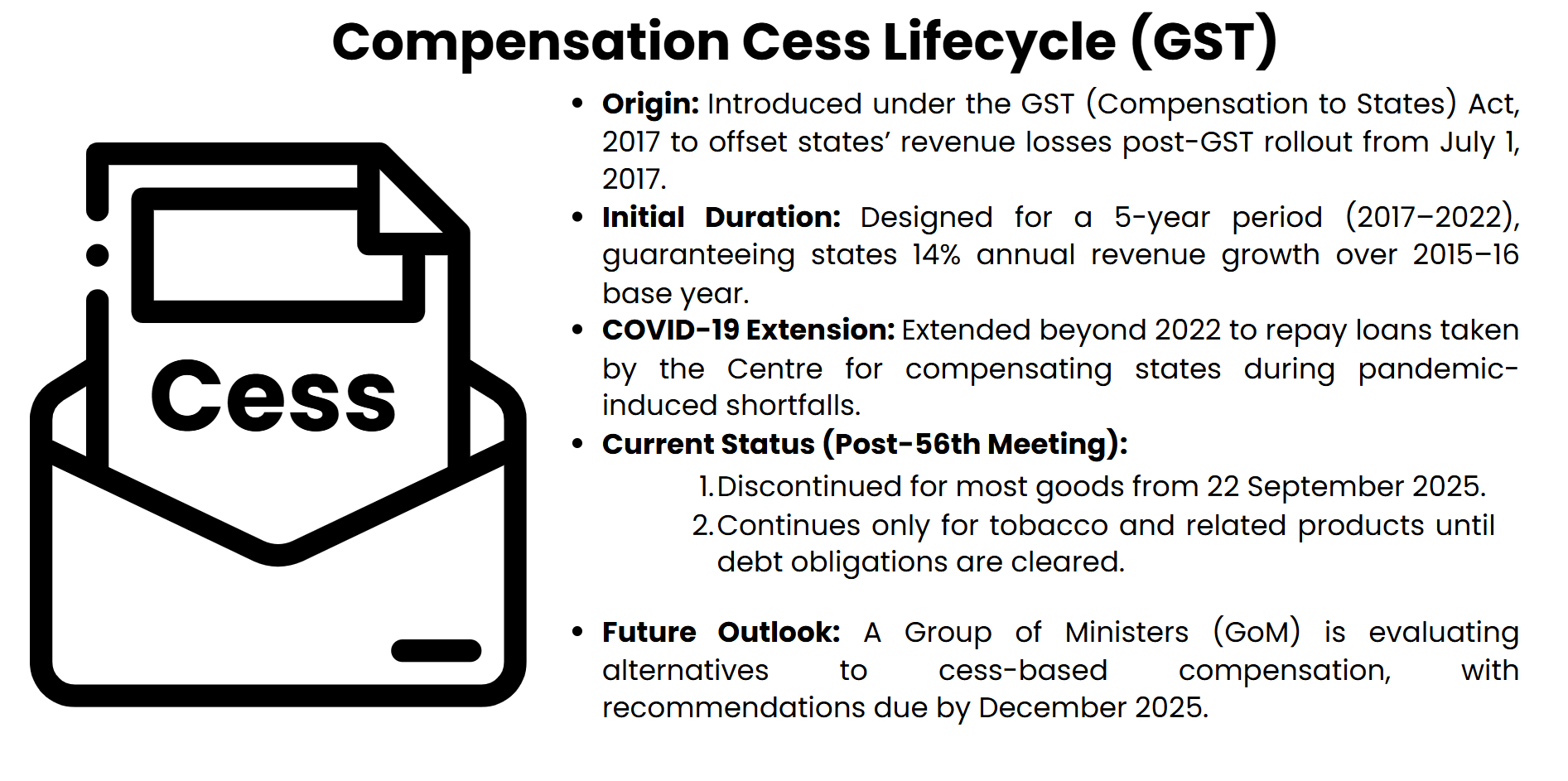

Compensation Cess

- The revenue loss by the states after GST was offseted by its introduction in the year 2017.

- Borrowing has increased to extend past 2022 because of COVID.

- Ended on most goods in Sept 2025; it is carried over on sin and luxury products.

- Institutional Reforms: GST Appellate Tribunal to be functionalised, inverted duty framework rectified and compliance measures streamlined.

|

The GST Council was established through the 101stconstitutional Amendment Act. It was constituted as of the 279A Article of the Indian constitution. The Council, which is the body that represents all states and the union territories and includes the Union Finance Minister, represents the cooperative federalism in the Indian system of indirect taxation. Since 2017, when it started, the Council would periodically hold meetings to discuss concerns of the sector, refinance compliance, and recalibrate tax rates out of varied economic dynamics.In September of the year 2025, the 56th GST Council meeting was a momentous event that would bring a lot of simplification into the GST organization of India. Some of the most impressive results that were achieved included the creation of a rate system that had two slabs, which was tested in a bid to increase transparency and minimise classification disputes. It is believed that by reforming, compliance costs will be reduced and that small and medium businesses, in particular, will benefit since the policies on taxes are now better aligned with developmental priorities. Besides this, the meeting has dealt with procedural bottlenecks, clarified input tax credit norms, and checked up on the status of the Compensation Cess. This article critically analyzes the institutional aspect of the GST Council, important decisions of the last council meeting 56th, bringing into perspective what the revised rate regime and cess policy would mean to the fiscal environment in India.

GST 2.0 - Complete Guide to Decisions of 56th GST Council

The GST Council is the constitutional institution that has the responsibility of determining the indirect tax system in India in the GST regime. It facilitates harmonization among the states and facilitates cooperative federalism.

Drafting and Development Constitutionally

Article 279A of the Indian Constitution was ranged in its 101st constitutional Amendment Act (in 2016) to set up the GST Council. It also has the Finance Minister as Chairman, Minister of State (Finance), and Finance Ministers in all states and union territories. It is also a federal structure of Indiathat provides the central government and the state government with the ability to shape GST policy, thus resulting in non-contentious decisions to be made. The Council has the mandate of providing recommendations concerning the rates of taxes, exemptions, and threshold amounts, and procedural reforms.

Functions and Decision-Making Powers

Changing GST laws through rate rationalization, exemptions, and administrative procedure is the main mandate in the Council. It also resolves inter-state contention and compliance bottlenecks. The decisions are made by means of several votes whereas the central government has one-third and the states have two-thirds of all the votes. Any resolution must have a majority of three-fourths to assure balanced representation and to bar unilateral domination.

Role in bringing together Indirect Taxation

The indirect tax system in India used to be disjointed prior to GST, since it had several taxes such as, VAT, service tax, and excise duty. The GST council has a key contribution of integrating these taxes in one regime, thus leading to the reduction of both cascading and the efficiency of the tax. It periodically adjusts the sectoral needs and economic variables in order to re-establish rates and ease compliance. This is a dynamic approach that enables the Council to rise to the challenges of fiscal policies and facilitate ease of doing business.

Fiscal Federalism and Institutional Significance

An example of such an Indian national determination towards fiscal federalism is the GST Council. It formalizes the communication between the Centre and states that balances national interests and regional demands. Its choices have effects on the income allocation, economic competitiveness, and welfare provisioning. Such a deliberative framework of the Council has also played a key role in addressing the controversial matters such as state compensation, anomalies around rates, and internet compliant systems.

The Highlights of the 56th GST council meeting

After a long and demanding journey of indirect tax reform, the 56thCouncil meeting represented a major landmark in reforming the Indian tax system. It brought with it simplifications with regard to structure, sectoral reliefs, and enhancements in compliance to make the whole process transparent and economically efficient.

Structural Reform: Two Slabs GST

The council passed a much-awaited reform, a much-awaited overhaul in the system of GST rate by combining the current four slabs (5, 12, 18, and 28%) in a two-slab framework. The updated framework consists and includes of a 5 percent merit rate of basic goods and services and an 18 percent standard rate on most other goods and services. Also, the sin tax was addedon sin and luxury goods.

Essential Sector exemptions

The significant triumph was the total exemption of GST on critical sectors. The tax net was exempted on life and health insurance policies, 33 life-saving medicines, necessary food products such as Indian breads and paneer, as well as UHT milk. These exemptions would be used to improve affordability and promote the welfare of the population, especially healthcare and food.

Rate cuts across major industries

The Council ratified a huge reduction in consumer goods and industry input rates. Products like hair priority, toothpaste, soaps, bicycles, and cookwares were transferred to the 5 percent slab. There were also decreases in taxes for agricultural machinery, such as tractors, threshers, and irrigation apparatus, which help sustain rural production. In the auto and building industries, GST on small cars and cement was reduced down to 18 percent by cutting demand levels and investment.

Compliance and Reforms in Institutions

In addition to the rate changes, the Council encoded procedural bottlenecks. It declared that the GST Appellate Tribunal will be operationalized by the end of 2025 in order to speed up the process of adjudicating disputes. The issue of inverted textile duty structure was also removed with measures carefully implemented to better digital filing. These reformation initiatives seek to improve the clarity of the law and limits litigation, thereby cleaning up the entire GST eco system.

New GST Structure and Impact on Sectors

A historic overhaul of indirect taxes in India came with 56thGST council, which was held in September 2025, with the revision bringing huge changes in the GST rate mechanism into the limelight. This simplification is meant to boost compliance, minimize classification conflict, and stimulate sectoral development.

Switch-Over to Two-Slab Construction

The preceding multi-tiered system of GST (5, 12, 18, and 28 percent) was substituted by the simplified two-slab structure of 5 and 18 percent (respectively): the essential items as well as services were taxed at 5 percent, whereas the standard items were taxed at 18 percent. Sin and luxury goods were taxed at a special rate of 40% which combined old cess-inclusive rates. This is hoped that too will result in less ambiguity in the classification and a more efficient tax administration.

The Boost in Sectoral Relief and Consumption

There was massive relief in fast-moving consumer goods (FMCG), agriculture, and construction industries. Products such as soaps, toothpaste, bicycles, and kitchenware were shifted to the 5% slab, hence being accommodated by consumers. The rate of disbursements was also cut on inputs used on agriculture, like tractors and irrigation equipments; so that the rural sector was still supported in ensuring that the rural people get opportunities. On the one hand, in building, reduced GST on cement and materials will decrease the costs of housing and increase the development of infrastructure.

Automotive/ Aviation Adjustments

The auto industry also had the gain in less GST imposed on two-wheelers and small cars whose engine capacities are less than 350cc and 18 percent tax, respectively. On the other hand, SUV vehicles and luxury cars moved into the 40-percent slab and substituted the previous mix of 28-percent GST and Compensation Cess. A further reclassification occurred in aviation with 5% remaining on the economy-class tickets, with business and first-class agreements taking the rate up to 18, from 12%.

Beverage and Health Sectors

Previously charged as tax, at 28 plus cess, the carbonated and caffeinated drinks now attract 40% of the GST. This action should deter the unhealthy consumption, but it is revenue neutral. On the other hand, the necessary health products like dental hygiene products and life-saving drugs were exempted or shifted to the 5 percent slab, which showed a welfare-based orientation.

Compensation Cess

Compensation Cess under the Goods and Services Tax (GST) regime was meant to counter transitional fiscal issues of the states after the transition to a single indirect tax, so this was to accommodate. It is still an important device in counterbalancing the dynamics of federal revenue.

Cause and Purpose

The Compensation Cess had been introduced by the GST (Compensation to States) Act, 2017, with its main purpose being the counterbalancing of losses in revenues by the state caused by the introduction of GST on 1 July 2017. The cess was set to last five years, which states would have guaranteed revenue growth of 14 percent/annum over their base collection year of 2015-16. This mechanism played a critical role in liaising the collective agreements among states to embrace GST, thus reinforcing cooperative federalism.

Scope and Applicability

The cess is imposed on luxury or sin goods. This can be applied on top of the normal GST rates in addition and is paid to the Centre. Notably, input tax credit (ITC) of Compensation Cess cannot be utilized to pay taxes on CGST, SGST or IGST. The exporters will receive refund on the cess they pay on goods that they export and at the same time remain neutral in international trade.

Extension beyond Initial Period

The cess was extended due to fiscal exigencies even though the initial five-year term expired in June 2022 (especially requirements to service loans obtained during the COVID-19 pandemic to reimburse states). According to 56thGST council meeting the cease will remain on tobacco and other related products, until the central government satisfies the liabilities. The cess will be scrapped from 22 September 2025 with regard to all other goods and services. Such a gradual withdrawal is an indication of the shift towards a leaner GST without losing fiscal discipline.

Limitations and Budgeting Future

Compensation Cess on a few items should be maintained so that debt servicing is not at the cost of key sectors. Its progressive phase-out is in line with the larger objective of the Council that being simpler about GST framework. But whether full withdrawal can be achieved depends on the state of the macroeconomic and even the elimination of the debt. The cess can therefore be seen as both transitional protection as well as specific fiscal instrument.

|

Goods and Services Tax (GST)

- Unified tax System: GST is a unified, destination-based indirect tax that supersedes various central, state taxes; VAT, excise duty, and service tax, since 1 July 2017.

- Constitutional Background: GST has been introduced by enacting the 101st Constitutional Amendment Act, such that in accordance with Article 366(12A), the tax is a tax on the supply of services or goods, except alcohol for human consumption.

- Dual Structure: India has a dual format of GST- Central GST (CGST) and State GST (SGST) on the intra-state dealings and Integrated GST (IGST) on the inter-state supplies.

- Multi-stage Taxation: It is charged at every level of value addition, that is, between manufacturing and retail, but input tax credit is not charged to avoid cascading effects.

- Digital Compliance: GSTN (Goods and Services Tax Network) will allow online registration, filing of returns, and authorize refunds such that there is a more transparent and simpler way of doing business.

- Economic Effect: GST has simplified the administration of taxes, helped increase the tax base, as well as enhanced revenue collection and the vision of a One Nation, One Tax, One Market.

|

Conclusion

The 56th GST Council meeting marks a landmark shift in the fiscal management of India, where a simplified two slab GST system was introduced, and specific sectoral changes were noticed. The Council has embedded its sense of equity, efficiency, and economic stimulus by rationalizing and providing tax exemptions on necessary goods and services. A future-facing tax environment meets the needs of the stakeholders by the operationalization of the GST Appellate Tribunal and procedural streamlining, indicates the receiving of a maturing tax ecosystem. The Compensation Cess being diminished in phases, in the meantime, indicates a pragmatic-fiscal consolidation and intergovernmental trust approach. All these decisions taken jointly demonstrate the changing role of the Council as an actively developing institution juggling national interests with federal autonomy. The GST council has been core to the design of an observerable Indian indirect tax regime that is transparent, inclusive, and geared towards growth. This momentum has to be nurtured in the future through further intensification of stakeholder involvement and institutional responsibility.