Key highlights:

- Rupee depreciation and capital outflow due to global tariffs

- Market-driven currency management by the RBI

- Help to exporters due to market diversification

- Balanced growth and stability demand

- Need of new Market

|

Exposure of rupee has been diluted by allowing tensions against rupee to tighten, and producers are making a lot in export, and RBI is withheld, and this has already proven its test by raising a red flag of creating inflation risk and this is not certain that the economy would be stable in the long run.

The declining, low-level value of the Indian rupee has now triggered an open criticism of the monetary policy of the Reserve Bank of India against the backdrop of a growing, tense tariff environment in the world that is sharply taking its place. With increasing trade protectionism, especially the so-called U.S. led tariff increases, the emerging markets such as India are subjected to greater currency fluctuations, outflow of capital, and inflation. In spite of all these, the RBI has resorted to a containment strategy, which has denied the central bank an aggressive role in the foreign exchange markets. The key questions about this strategic silence are whether such action is intended to protect foreign reserves, leave improper corrections to the market, or indicate trust in macroeconomic fundamentals by the central bank.At the same time, the weak rupee offers an ironic benefit to the Indian exporters. A low currency will improve competitiveness in exports because it makes products cheap to foreign consumers, and this will counteract the negative implications of tariffs. This dynamic recalls the vexed trade-offs faced in both remaining stable in currency and controlling inflation and export-led growth. The article discusses these tensions in four major dimensions, including: the international trade environment, policy calculus within RBI, sectoral benefits of a weaker rupee, and the economy-wide risk associated with long-term depreciation. Descriptive analysis of these dimensions, as connected together, would explain a three-dimensional picture of India in a turbulent international arena and its effects on trade, development, and financial stability.

World Trade Friction and Rupee deflation

Early in the year 2025, the Indian rupee also underwent a significant depreciation as international trade began encountering increasingly hostile trade conditions. This kind of crash is brought about by a compound extrinsic shock, changes in policy and data regarding the perception of investors that change the macroeconomic climate of India.

Increasing Tariff Measures and International Uncertainty

The revival of protection trade policies,especially during the U.S. administration, has triggereda wider response. By January 2025, the U.S had imposed harsh tariffs on imports from most of its trading partners, including Canada, Mexico, China, and this spillover effect was felt by India since its exportations and connection with its supply chain were exposed. These actions destroyed international trade movements, caused investors to lose confidence, and caused a flight of capital to risk-sensitive economies. Rupee, among other Asian currencies, was adversely affected when foreign portfolio investors shifted their assets to safety havens.

Lacking Structure in the Indian External Sector

The reliance of the rupee was worsened by the existing current account deficit and reliance on foreign goods and raw materials, particularly crude oil, which India heavily imports. Even when global oil prices temporarily fell, the trade balance narrowed since export growth was rather slow and the amount of import bills grew. Foreign portfolio outflows further enhanced the depreciation and escalated when monetary conditions remained tight in the more advanced economies. Such structural weaknesses, coupled with exogenous shocks, formed a virgin soil of currency instabilities.

Policy shift and Market Signaling of RBI

The Reserve Bank of India embraced a flexible exchange rate regime under Governor Sanjay Malhotra, as opposed to the earlier regime of active intervention. By stating that the central bank would grant the rupee some breathing room to adjust to market forces, the central bank is more interested in the long-run stability of the currency than short-run volatility.

Comparative Resilience and Standpoint

The depreciation, however, made the rupee fairly stable when compared to other emerging market currencies as it only fell by 1.8% against the U.S. dollar in the first quarter of 2025. This humble fall suggests that India possesses solid domestic fundamentals (including a sound GDP growth and even domesticated inflation). However, analysts suggested that the rupee will continue, to depreciate as long as trade tensions continue, and liquidity is limited on a global scale.

Strategic Silence: is it Calculated or Risky?

There has been a debate among economists and market researchers that this act by the RBI is a cautious response. Such tactical silence is the transition of the philosophy of money, the diversity of currency, and macroeconomic prudence.

Change in Philosophy of Currency Management

Under Governor Sanjay Malhotra, the RBI has reneged on its previous interventionistic policy, and the rupee has been delivered to the mercies of the market. This is unlike the extremely constrained exchange rate regime that was favored by his predecessor, Shaktikanta Das. Analysts believe that this reduced activity of the RBI is intended to save the foreign exchange reserves and avoid crippling liquidity shocks. The interest of the central bank is to align the real effective exchange rate (REER) of the rupee to the fundamentals by accepting gradual depreciation, which will widen the stability divergence in the long run.

Liquidity Trade-offs versus Inflation

Silence on the part of the RBI may seem passive, but it shows a trade-off. The sale of dollars aggressively to support the rupee in late 2024 exhausted forex reserves worth up to almost 79 billion dollars and sent domestic liquidity into deficit. The present policy, on the other hand, does not overburden depletion and lets RBI, instead, concentrate on inflation targeting and bond market operations. The negative aspect is, however, that there is a risk of this, and that risk is the upward movement of the imports; they would be oil and electronics in particular, and this would make the monetary policy difficult, and it would take the consumer’s buying power away.

Confidence in the market among investors

A subdued reaction by the RBI is also a sign to international investors that India is intent on an elastic exchange. It goes hand in hand with IMF recommendations and increases the credibility of India in world financial markets. However, the apparent absence of help to the rupee could also destabilize short-term investors, not least because of falling foreign portfolio flows and increasing U.S. interest rates. In the last quarter of the financial year 2024-25 rupee saw its highest fall in the past two years.

Strategic Silence: Two-Sided Sword?

Finally, the silence adopted by the RBI cannot be regarded as a strictly passive stance that would be completely safe. It is a recalibration of strategy to think in the long term, as opposed to the short term. But in the scenario where inflation rises and global uncertainty increases, then the RBI must act bolder. The status quo, although wise in principle, needs to be effectively monitored to prevent unintended surprises in trade, investment, and consumer temperament.

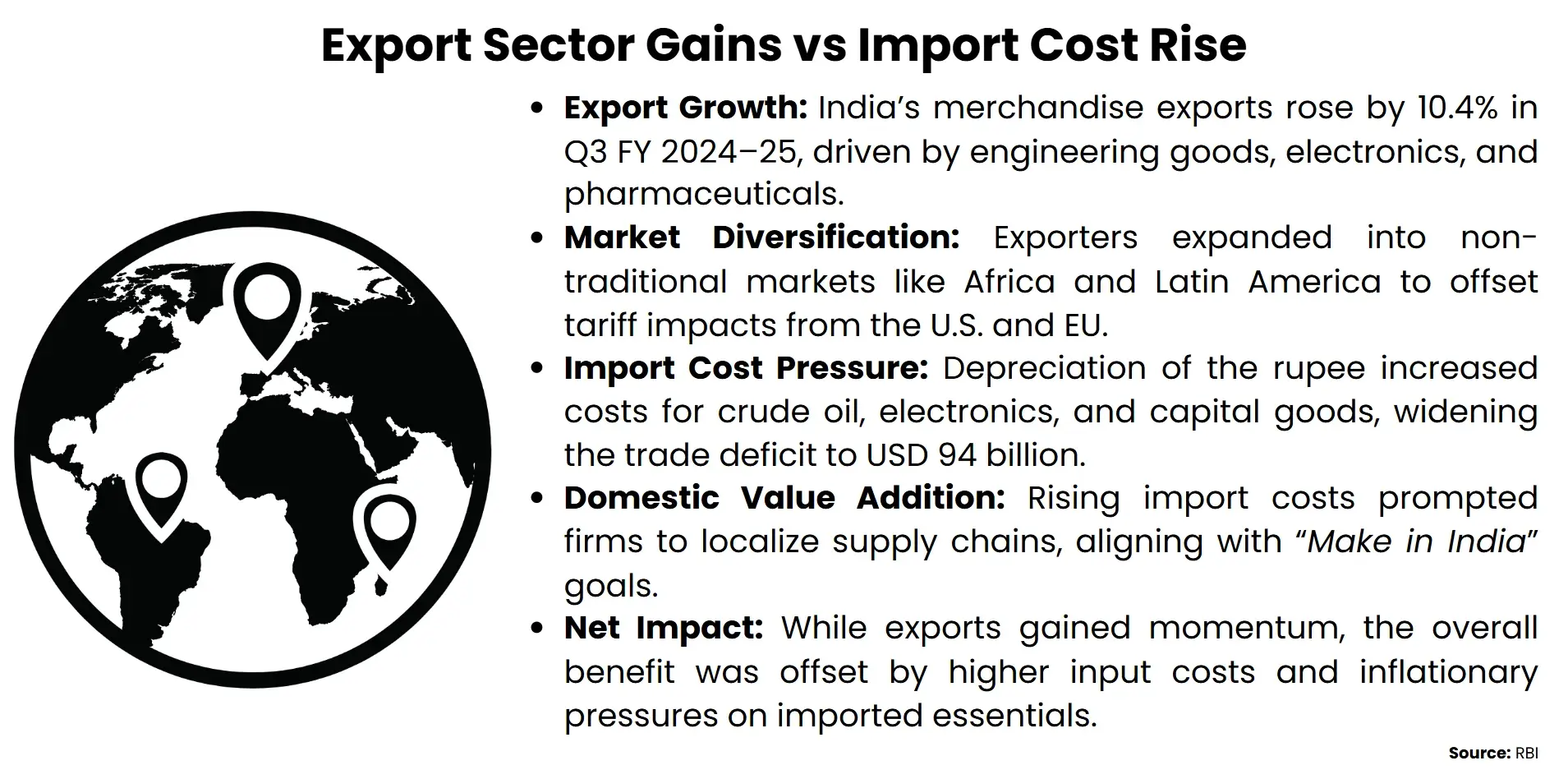

Exporters Advantage

With the depreciation of the Indian rupee against the global tariff stress and outflow, the economic future in 2025 has become unaffordable. In the challenges, exporters have obtained a strategic advantage.

Competitorsin the international market

This is because a depreciated rupee has a direct positive correlation with the price competitiveness of Indian goods in the global markets. Since the exchange rate of the rupee is close to 88.15 rupees relative to the U.S dollar, exporters can sell at reduced prices without reducing their profits. This is a special advantage in price-responding industries like textiles, agricultural goods, and engineering products, where minor price differences may determine purchaser behaviour.

Diversification outside the conventional markets

With increasing tariffs in the United States, the biggest United States export market, exporters are turning to African, Southeast Asian, and Latin American emerging markets. This change relies on the depreciation of the rupee,which is helping to make Indian products more attractive to more economies. The FIEO noted that this is time to explore more markets apart from the U.S.

Incentive for domestic value addition

Food supply chains were forced to rethink their strategies due to the currency movement. Those exporters who depend on imported inputs (electronics, gems, and petroleum products) have increasing costs that are partially counterbalancing the advantages of a weaker rupee. Most companies are reacting to this by investing in domestic value addition in order to decrease the level of imports. This not only increases profitability, but it also fits with the Supreme Indian objective of self-reliance and manufacturing competitiveness as part of the Make in India project.

Winners and Constraints in the sectors

At the same time as the depreciation provides tailwind to a host of successfully export-based sectors, but it has unequal benefits. This does not provide significant net gains in areas with high import intensity or operation costs in dollars. Besides, exporters who protect their currency hedge by use of forward contracts are not assured of full utilization of the rupee advantage. Therefore, although the macroeconomic story leans towards those who prefer to export, firm-level performances are attributed to the cost structure, market agility, and strategic positioning.

Balancing Act

The fall of a rupee is a cautious step taken by the RBI. On the one hand, it provides gain to exporters in the short run; at longer run, systemic risks are involved in the macro economy.

The Imports and the Inflation Effect

Major imports will rise in prices as the value of the rupee decreases. India is almost purely a fuel importer, importing more than 80 percent of its oil demand, and the price pressures on the world, aggravated by the Middle East unrest, have increased the cost of fuel domestically. This crossing rail impact increases transportation and manufacturing costs, and eventually overburdens the customers with elevated retail costs. The inflationary spiral threatens to erode the domestic household purchasing power and make it challenging for the inflation-targeting mandate of the RBI.

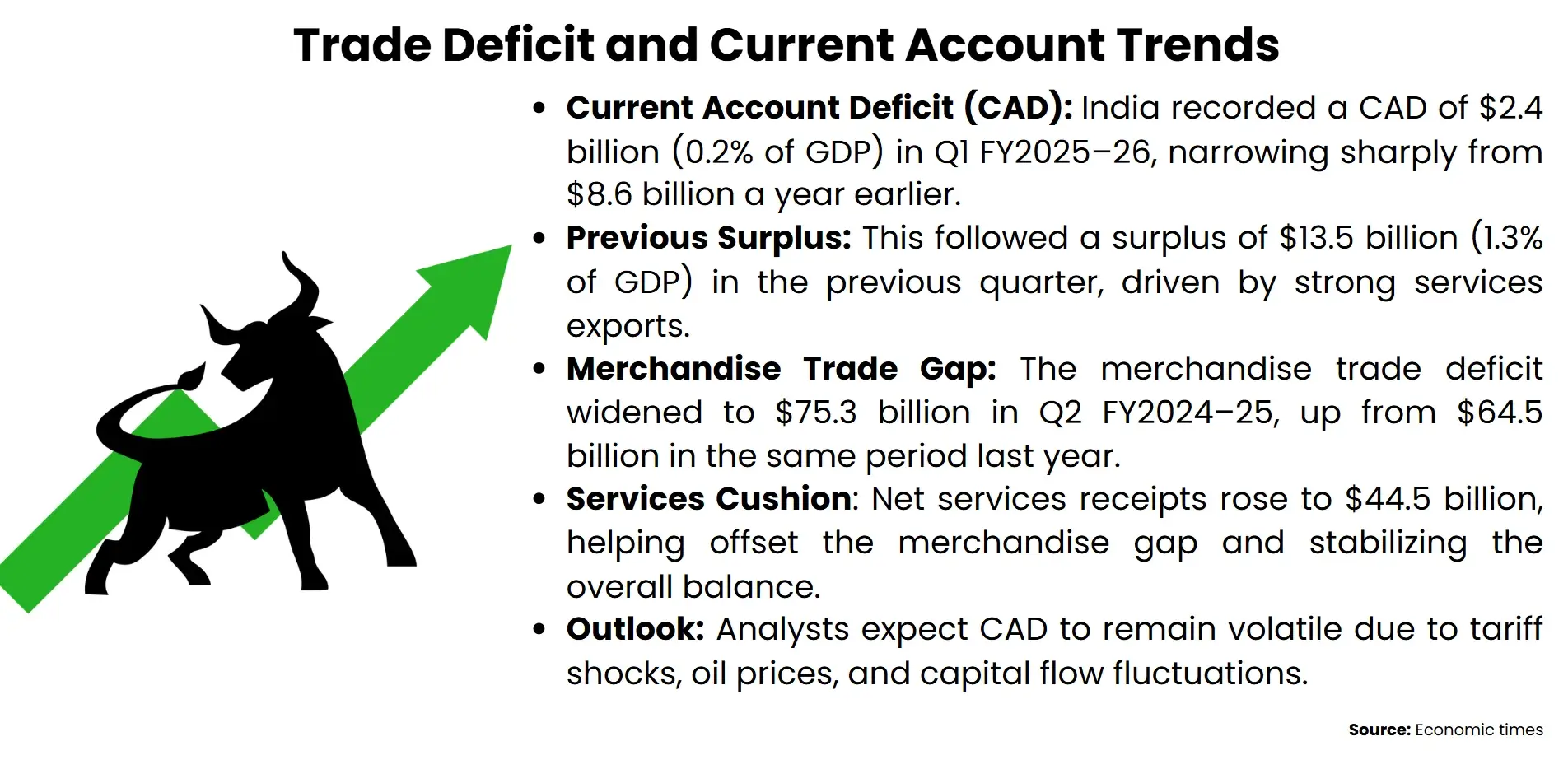

Widening Trade and Current Account Deficit

Export can be advantageous because the currency can be depreciated, but it is not clear what the overall impact on the trade balance will be. The import bill of India has been escalating faster than the export earnings due to high demand for goods such as energy, gold, and capital. Possibly, a long rupee slide deteriorates the current account deficit. Such disequilibrium increases external fragilities and can lead to credit rating anxieties, on8to the sovereign cost of borrowing and investor sentiment.

Capital Flight and Financing Market Volatility

Currency risk is sensitive to foreign portfolio investors. The weakening of the rupee, combined with the slow pace of U.S. rate cuts and a risk-averse attitude globally, has resulted in short-term outflows of capital out of Indian stock markets and even the Indian bond markets. This is because in July 2025 itself, FPIs pulled out over rupees 2,300 crore from domestic markets. Such volatility kills the stability of financial markets and may further erode the rupee and trigger a vicious circle of demands on the monetary authorities to step in.

Policy constraints and reserve management

This reserved nature of the RBI is an attempt to revive foreign exchange reserves lost in previous interventions. However, this limitation eliminates its ability to counter episodes of great depreciation. By August 2025, the RBI hasunwound 23 billion dollars in its forward book and is still buying the dollar in the spot market. This two-sided policy would squeeze liquidity further and suppress rupee recoveries, and make the policy space to doubt whether the central bank will respond to any other crisis succeeding it.

Conclusion

A weakening of the Indian rupee due to global tariff threats endangers and complicates economic policyandrequiresa policy intervention. Even though the exporters attain the choice of competitive prices, overall, macroeconomic problems of rising cost of imports, rise in prices, and loss of funds in the economy, leave weight to the product of ineffective currency, which will not last long. The reticence of the Reserve Bank of India is arguably a market term for an exchange-rate management figure, but the reticence of the bank is one to be carried with some worries in a different environment where inflation is to be controlled and investors are to be entrusted. This fluctuation in the rupee will put India to test of its economic credibility and stability in the global arena. It is necessary for future financial choices to balance a short-term payoff with an abiding exposure to currency flexibility. In that sense, the currency movement of the rupee is not only a financial metric but also an indicator of the changing Indian position in world trade dynamics.