PAYMENT AGGREGATORS V/S PAYMENT GATEWAY

What is a Payment Gateway?

- A payment gateway in India facilitates online transactions by securely authorizing and processing payments between customers and merchants.

- Functionality: It encrypts sensitive transaction data, ensuring secure communications between the customer’s bank and the merchant’s bank. Payment gateways can also support various payment methods, including credit/debit cards, net banking, UPI, and wallets.

- Regulation: Payment gateways in India must comply with regulations set by the Reserve Bank of India (RBI) and other governing bodies.

- Examples: Razorpay, PayU, Instamojo, CCAvenue.

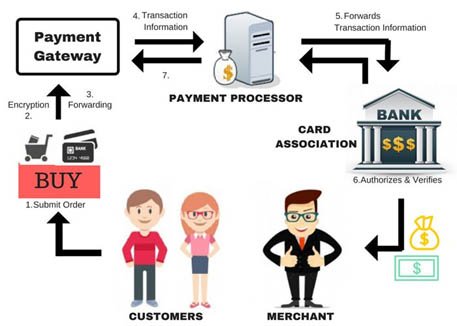

HOW DOES A PAYMENT GATEWAY WORK?

1. Integrate a Payment Gateway: Once your online store is set up, choose a payment gateway provider and integrate it into your checkout process. You can customize it to accept various payment methods.

- Integration Options:

- API: For custom websites.

- Plugins: For platforms like WordPress and Shopify.

- SDK: For custom mobile apps.

2. Customer Makes a Purchase: The customer selects items and chooses a payment method, entering their card details. The payment gateway securely handles this information.

3. Redirect to Payment Gateway: The customer is directed to the payment gateway to enter their payment details. The gateway encrypts the data and performs fraud checks before processing the transaction.

4. Authorization and Response:

- The acquiring bank checks the transaction's validity and contacts the issuing bank for approval.

- The customer is notified of the transaction status (approved or declined).

5. Settlement: After approval, the acquiring bank transfers the funds to the merchant, usually within a few business days. The customer receives a confirmation of their order.

PAYMENT AGGREGATOR

PAYMENT AGGREGATOR

- Payment aggregators allow businesses to accept payments without the need for a traditional merchant account, offering a simpler setup process.

- Functionality: They bundle multiple payment processing services, enabling merchants to accept various payment methods through a single integration. This makes it easier for small businesses and startups to get started with online payments.

- Fee Structure: Aggregators typically charge a percentage of the transaction amount, along with some fixed fees.

- Examples: Paytm, PhonePe, Google Pay, MobiKwik.

KEY FEATURES

- Seamless Onboarding and Sub-Merchant Accounts: Payment aggregators enable businesses to create sub-merchant accounts, making it easy to manage payments for multiple stakeholders.

- Secure Payment Processing: They invest in robust security measures to protect sensitive payment information, including data encryption and tokenization.

- Fraud Detection and Prevention: Payment aggregators analyze transaction patterns and use machine learning to identify fraudulent activity, complying with RBI regulations.

- Multiple Payment Options: They provide a range of payment methods, ensuring a smooth experience for customers.

- Fast Settlements: Payment aggregators often offer instant or same-day settlements, helping businesses manage cash flow effectively.

- Seamless Checkout Experience: They create a user-friendly checkout process to minimize transaction drop-offs.

- Customer Support: Payment aggregators have dedicated support teams to assist customers and merchants with queries and issues.

HOW PAYMENT AGGREGATOR WORKS?

- Onbording Merchants: Businesses create a merchant account with a payment aggregator, which processes all transactions through a nodal account with a bank.

- Payment Window: Customers select a payment method and enter their details, which are tokenized for security.

- Transaction Processing: The aggregator processes the transaction in the background, communicating with banks and payment processors.

- Fraud Check: Card companies perform fraud checks based on customer behavior before approving or denying the transaction.

- Customer Bank Processing: The customer’s bank verifies the transaction and sends back the approval status.

- Funds Request: Once approved, the payment aggregator's bank requests the funds from the customer’s bank.

- Settlement: At the end of the day, the aggregator settles all transactions on behalf of the business, with options for instant settlements available.

TYPES OF PAYMENT AGGREGATORS

- Bank Payment Aggregators: Operated by banks, they facilitate online payments but require more resources for setup and integration. They often come with higher costs and less flexibility for smaller businesses.

- Third-Party Payment Aggregators: Non-bank aggregators that require RBI authorization. They are typically more affordable and easier to integrate, making them suitable for small businesses, offering features like sub-merchant management and analytics.

WHAT SHOULD BUSINESSES CHOOSE?

- Selecting a payment gateway or a payment aggregator depends on the specific requirements and preferences of your business.

- If you require a simple and secure solution for card-based transactions, a payment gateway might be adequate.

- Conversely, if your business requires you to enable multiple payment options, you can opt for a payment aggregator, which offers various payment methods, along with access to additional benefits such as robust customer support, and comprehensive business insights.

Note: Connect with Vajirao & Reddy Institute to keep yourself updated with latest UPSC Current Affairs in English.

Note: We upload Current Affairs Except Sunday.

Note: Connect with Vajirao & Reddy Institute to keep yourself updated with latest UPSC Current Affairs in English.

Note: We upload Current Affairs Except Sunday.